Posted September 23, 2022

By Sean Ring

The BoJ Blinks… Or Did It?

Happy Friday!

I wanted to write about something cheerful, but I couldn’t find anything.

So let’s stick to the unraveling currency markets, which seem to be ground zero for our current economic woes.

I’ve mentioned Japan a few times in the past weeks, and that’s much more often than usual.

But what’s going on with the yen is a once-in-a-generation event that requires our attention.

If there’s one thing I’ve never understood, it’s why the yen is considered a “safe haven.”

It seems the Bank of Japan’s sole mission is to destroy its currency. So why traders pile into it at the first sign of trouble always bemused me.

Right now, it’s the last place on earth you want to be.

In this edition of the Rude, I’ll talk about intervention and why it didn’t work this time.

Kuroda-san Took a Knife to a Gunfight

Here you can see Haruhiko Kuroda, the Governor of the Bank of Japan (in the hat), intervening in the market (the bald guy):

Of course, the Japanese would have none of that.

They think the transaction was more like this:

My point is that a knife or a ping simply wasn’t good enough.

The last time anyone felt this sort of crushing disappointment was Mrs. Ring on our wedding night.

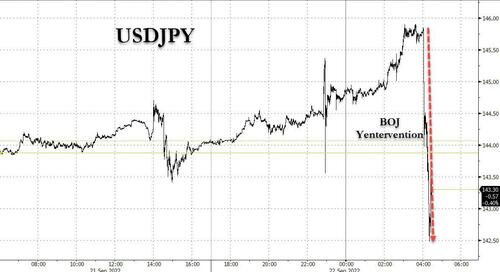

The Charts

ZeroHedge dubbed it the “Yentervention,” and I laughed for about a minute.

The problem with any government’s intervention in any market is that it better work.

And this intervention looks like a failure of epic proportions.

Here’s what the Yentervention looked like:

Credit: ZeroHedge

The BoJ moved the USDJPY about 1.1% from 145.50 to 142.50.

So it was a nothing-burger.

A few weeks ago, I wrote “Searching for Bobby Rubin,” wondering if the US Treasury would intervene in USDJPY like it did in 1998.

Let’s compare the move:

Yes, this chart is over a much longer period.

But Rubin’s initial intervention sent the USDJPY from 147 to the mid-130s.

It was an enormous move.

And Rubin was reluctant to make it, to begin with.

From that Rude:

And yet, the yen continued its descent against the dollar.

By June, though, the stoic Secretary had had enough.

Rubin was worried that an unsuccessful intervention in the currency markets would hurt American credibility.

But Rubin decided to act after a meeting with Greenspan, Summers, and Assistant Treasury Secretary Timothy Geithner (yup, him, too).

Rubin bought about $2 billion worth of yen, sending USDJPY from 147 to the mid-130s, an enormous move in the currency market.

Rubin was right to worry but smart to act decisively.

Kuroda-san doesn’t seem to have done either.

ZeroHedge predicts the USDJPY will trade at 150 within weeks.

This is disastrous for Japan’s import-dependent economy.

The Implications of Intervention

I wish governments would stay out of currency markets altogether.

But that’s not going to happen anytime soon.

A few weeks ago, Mihai Macovei over at Mises Wire wrote a peach of a piece titled, “Government Intervention into International Currency Exchange Rates: Japan as a Case Study.”

I can’t recommend you read it enough.

I’ll print the conclusion for you here, though, as I’m sure it’ll be beer o’clock soon where you are. The bolds are mine.

The equilibrium exchange rate between two currencies is given by their purchasing power parity—i.e., the ratio of the purchasing power of each in terms of other economic goods.

Any attempt to move the exchange rate from its market value through government intervention is likely to be undone by market arbitrage, which restores the exchange rate to its purchasing power parity.

A long-lasting change in currency value can take place when governments use monetary policy levers to adjust interest rates and the money supply.

In this case, the change in foreign exchange rates mirrors the movement of domestic prices and alters the trade balance, as Mises explained.

However, monetary policy interventions introduce other distortions into the economy which can have severe economic consequences, as illustrated by Japan’s lost decades after the Plaza Accord.

What the theory says is this: don’t bother intervening. The market will correct you.

In practice, Rubin’s intervention worked only because the market took it very seriously and started to reprice itself accordingly.

Kuroda-san’s intervention is too light to matter.

Not only that, but the Bank of Japan reiterated its ultraloose monetary policy and its aim of keeping the 10-year JGB yield at 0%.

JGB stands for Japanese Government Bond.

This flashed up on Bloomberg after the intervention:

- *BOJ'S KURODA: NO NEED TO CHANGE GUIDANCE FOR 2 OR 3 YEARS

So there will be no follow-through, nor any threat of such.

Hmmm… that seems a bit fishy. Keep that in your back pocket for a minute.

As for the second highlighted bit about the Plaza Accord, I refer to Macovei’s piece:

High budget deficits together with buoyant domestic demand swelled the [US] trade deficit, producing the famous 1980s “twin deficits.” In reality, the exchange rate was not the problem, but US fiscal profligacy and excessive money supply expansion, which exceeded 12 percent in 1983.

Instead of fixing domestic policies, the US government talked Japan and Germany into manipulating their exchange rates and increasing domestic demand.

As Ludwig von Mises put it so aptly: “What governments call international monetary cooperation is concerted action for the sake of credit expansion.”

Following concerted interventions by central banks, the yen appreciated from about 240 units per dollar in September 1985 to 153 units in 1986.

By 1988, the yen had almost doubled in value to an exchange rate of 120 units per dollar.

Many analyses, including International Monetary Fund reports, concur that the significant government-driven appreciation of the yen sowed the seeds for Japan’s subsequent long-lasting economic debacle.

In the first half of 1986, as Japan’s exports collapsed following the yen’s appreciation, the economy entered a recession.

The BoJ’s sales of dollars also squeezed the money supply and domestic demand.

The authorities overreacted and introduced a sizable macroeconomic stimulus, cutting interest rates five times, by a cumulated 3 percentage points, by 1989.

A large fiscal package was introduced in 1987, even though the economy was already recovering.

Credit growth then surged, fueling a stock market and real estate boom that burst in early 1990 and triggered almost three decades of dismal economic performance.

From this point of view, you can see why the Japanese may believe the yen is too strong, even now.

Considering our earlier point that the intervention was weak and policy hasn’t at all changed, did Kuroda-san not make a mistake?

Perhaps.

However, I’d remind the BOJ that this isn’t the 80s, and desperately needed oil isn’t $10 per barrel.

Remember, the Japanese need a yen that can buy the dollars required to pay for imported energy.

But that makes Japan’s renewed enthusiasm for nuclear power all the more understandable.

Wrap Up

So the BOJ wimpily intervened in the foreign exchange market for show.

The result is that dollar-yen may pause for a bit before it continues its ascent to 150.

But Japan isn’t all that interested in a strong yen anyway.

So this might be the very definition of kabuki theatre.

Nothing is as it seems anymore, is it?

With that said, forget about the markets for a few days, and have a wonderful weekend!

King: “It Can’t Happen Here”? Hey, It Just Happened Here!

Posted July 25, 2024

By Byron King

Nothing is Biden’s Fault

Posted July 24, 2024

By Sean Ring

The Democrats’ Dilemma

Posted July 23, 2024

By Sean Ring

Harris/Obama 2024?

Posted July 22, 2024

By Sean Ring