Posted October 25, 2022

By Sean Ring

VIEs, ADRs, and SPACs

- Acronyms, acronyms, everywhere…

- Are you buying Chinese stock on the NYSE?You probably don’t own anything but dust.

- ADRs and VIEs are entirely different structures.

This Rude’s main bits came from an earlier piece written on August 9, 2021. I wanted to update it, considering what’s going on in China.

If you haven’t read about it, President Xi has crowned himself Emperor Xi. This has wreaked havoc on Chinese stocks, especially in Hong Kong.

Shanghai stocks haven’t fared much better:

Back in August 2021, Chinese internet stocks listed on the New York Stock Exchange got hammered.

I had wanted to break down the structures that make it so easy for the Chinese Communist Party (CCP) to take American money and just set it on fire.

According to Stock Market MBA, 249 Chinese companies are listed on a U.S. stock exchange, either directly or as an ADR.

This guide will help you understand their listing structure.

Tread carefully if you dare to invest in China at all.

VIEs

Little did I know, and perhaps I'm at fault for not recognizing this, but the structure of Chinese internet stocks on the New York Stock Exchange is not in the form of ADRs (American Depositary Receipts). They are in the form of variable interest entities (VIEs).

Sometimes, VIEs go by their maiden name: SPVs or Special Purpose Vehicles.

Perhaps you’ve heard of them...

That may or may not mean something to you, but the last entity that famously used SPVs was a little company called Enron.

It's amazing how this works.

The reasons executives use VIEs are that China forbids foreign ownership of many of its companies, and US investors want access to China’s growth rates.

It's a ridiculous deal.

But Wall Street has this unbelievable penchant for coming up with solutions to these issues.

After all, Chinese companies need American capital, and American investors have been chasing yield for years now, so they want Chinese equities that outperform.

According to the South China Morning Post (Hong Kong’s leading English newspaper):

By one estimate, more than 100 VIE companies now command about US$4 trillion of capitalization in MSCI China Index. US-based investors could hold as much as US$700 billion worth of them, according to a government report in July.

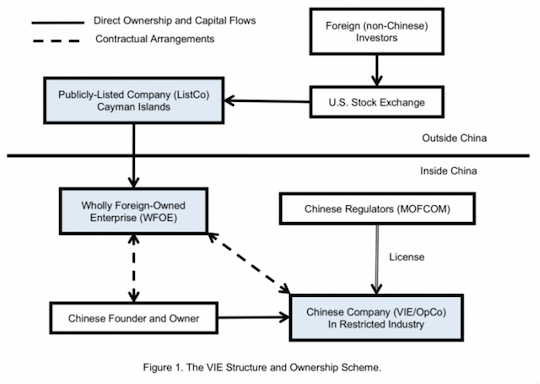

So they came up with this ridiculous structure. Here’s a schematic:

Credit: https://www.corpgov.net/wp-content/uploads/2017/12/VIE-Shell-Game-e1513300211535.png

{kind=link}

What happens is that American investors buy that stock on the New York Stock Exchange during its IPO phase. Then that company deposits that money in a wholly foreign-owned enterprise inside China.

The Chinese founder and owner of the Chinese company in that restricted industry have contractual arrangements with that wholly foreign-owned enterprise.

The Chinese regulators regulate the Chinese company.

But American investors don't actually own the company in China.

It's ludicrous.

Of course, the CCP is very happy about that because they don't want foreign ownership, but they want the capital. So they make out just fine.

And as long as the Chinese government doesn't pull the rug out from American investors as they did a couple of weeks ago, American investors get their growth.

But of course, this blows up spectacularly when China turns its very profitable companies into non-profits overnight by government decree.

Not only are regulators ignoring this, but the global accounting community is also. According to both IFRS and US GAAP, when you look up the listed VIEs, you get the Chinese companies’ financial statements.

Let’s contrast this structure with American Depositary Receipts.

ADRs

You may have heard of the American depositary receipt, but let me explain them quickly.

It's understandable to think that these Chinese companies were in the form of ADRs because we have many American depositary receipts.

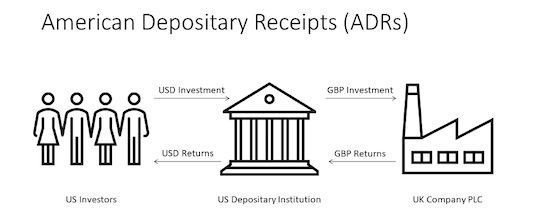

ADRs are dollar-denominated claims on foreign assets. As you can see from the diagram below, a UK company like Vodafone, which does have an ADR on the New York Stock Exchange, decides it would like access to American capital.

It’s crucial to note that ADRs were developed when most investable wealth in the world was in America.

(The only thing more embarrassing than America being as rich as it was, is how it lost its lead in being the world's richest nation.)

Credit: Sean Ring

Foreign companies just thirsted for American capital.

US depository institutions such as Bank of New York Mellon, Bank of America, or State Street took a lead role.

Those banks are exceptionally good at custodial activities.

So they would purchase the London-listed shares of Vodafone.

Then they’d issue on the back of those shares a paper called the ADR that says ten shares of Vodafone equals 1 ADR.

So legally, you own a piece of Vodafone and get your capital gains and dividends converted to USD.

Of course, you have FX risk, but the structure is very legal and tight. And you indeed have a claim on those assets in the form of ownership.

With variable interest entities, you do not.

And it's funny because this is precisely the kind of shell game that Enron played before it blew up. It used to park its losses offshore, and no one could see its financial statements because Enron didn't consolidate them in its company financials.

In this situation, however, and this is a massive failing on the part of the regulators, the Chinese stock is registered as ownership even though you don't actually own anything.

You just kind of have a stock that is a VIE that is not ownership. It's all very frightening, to be honest with you.

Since we've just talked about VIEs and ADRs, let's talk about SPACs.

SPACs

SPACs?

I don't want to confuse you with acronyms today, but you would have read about SPACs already.

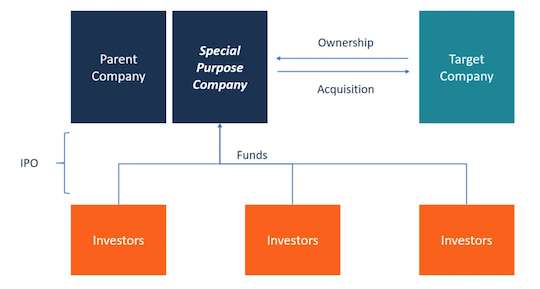

A special purpose acquisition company (SPAC) is a corporation formed to raise investment capital through an initial public offering (IPO).

Once the company is formed, it has another 18-24 months to buy another company.

Now, again, this is another ridiculous structure. We have seen many recent lawsuits because the “company” has no history.

The only thing it has is a management team.

It has no track record for it to run on.

You're just asking investors to give you money to make an acquisition later on.

By the way, those investors don't even know what that acquisition will be.

Investors like Chamath Palihapitiya are big fans of this structure.

Yes, if you get in early and people don't know what's happening, you'll make a lot of money.

But now, there are many lawsuits regarding SPACs because SPACs don't return anywhere near the money that investors expect them to return.

Wrap Up

So, between variable interest entities, American depositary receipts, and SPACs, we have an alphabet soup of potential fraud if you don't know what you're dealing with.

Stay safe out there because it is perilous, and your regulators are not protecting you.

Have a great day.

Keep Calm and Tariff On!

Posted April 03, 2025

By Sean Ring

Private Equity’s Latest Target: Your Parents

Posted April 02, 2025

By Sean Ring

Gold to the Moon, Crypto to the Morgue

Posted April 01, 2025

By Sean Ring

TANKED! Trump’s Tariff Update

Posted March 31, 2025

By Sean Ring

Your Wallet: Fill ‘Er Up!

Posted March 28, 2025

By Sean Ring