Posted April 08, 2025

By Sean Ring

From Taxed to Relaxed: Retire Like a Pro

I wrote an article titled “Private Equity’s Latest Target: Your Parents” a few days ago, and the mailbag has been lively. Thank you to Andrew R., Kristen W., Jim S., Gary H., Damon C., and a subscriber who wrote a touching story about his mother-in-law, but didn’t sign his name.

I’d print your responses, but they were so effusive in their praise, it’d seem self-serving. However, Andrew R. wrote this at the end of his:

I thank you for the article and I commend your ability. There is, however, one disappointment I had with the article. Normally, you provide (or imply) solutions to the problems you write about, but not in this case. In that respect, the story was anticlimactic and atypical of what I have come to expect from you.

Andrew, you’re right. I didn’t provide any solution other than to get the word out.

This, combined with the Trump Administration’s alleged hijacking of the stock markets, has me thinking some of you may be worried right now. I think I can help you here.

In this edition of the Rude, I’ll present sound steps that I’ve used to put my family and me on sound financial footing. To mix flying metaphors, your mileage will vary depending on how much runway you have.

First, a disclosure: I don’t know your financial situation, so please don’t take this as financial advice. These steps worked for me, but feel free to replicate anything you think will work for you.

Hire an accountant.

This is always my first piece of advice. I never do my taxes on my own, and I always ask my accountant what’s tax deductible.

Before you recoil, know that The Donald wants to cancel income tax entirely. Also, a “heavy progressive or graduated income tax” is the second plank of The Communist Manifesto.

So don’t feel bad about reducing your payment to the IRS to the absolute minimum. Never evade tax; they’ll catch you and hang you out to dry for it. Do avoid tax, which is entirely legal.

Set up a deal in which, in the early years, the accountant reduces his fee in exchange for results and loyalty. As long as the accountant proactively reduces your tax bill, there’s no need to switch.

Don’t cut menial expenses; cut taxes and mortgage payments.

This goes hand-in-hand with my first point. That Starbucks coffee you drink every day isn’t what’s causing your financial woes. Paying federal income tax, state income tax, local income tax, property tax, sales tax, mortgage payments, and the other innumerable fees Americans charge is hurting you.

How can you fix it? Years ago, Tim Ferriss talked about “geoarbitrage” while inventing “lifestyle design.”

First, let’s talk geoarbitrage. It involves earning in a strong currency while spending in a weak currency. For instance, you could work for a firm based in NYC, earning NYC wages, while residing in the Yucatan or Medellin, Colombia. If you prefer not to leave the U.S., that’s fine. You can earn NYC wages while living in eastern Pennsylvania or the South. The key is to capitalize on high-inflation areas while residing in low-cost regions.

How do you figure out how to do that? That’s where lifestyle design comes in.

When you have time on a Saturday afternoon, grab a pen and paper and head to your happy place. That could be your kitchen table, patio bench, or favorite coffee shop. Take your spouse with you. Dreaming together is a lot of fun. Then, don’t hold back: go nuts.

Write down your dreams. Want a fabulous apartment overlooking the sea? Great. Want a farmhouse in the flatlands? Great. Want to chill in a city pied à terre? Fantastic.

And here’s the thing: don’t compromise. Argue it out (politely). One of you is going to win. The other has to be on board with the decision. The trick is to keep talking and talking until you get all your dreams on paper. That alone will be the basis of your action plan.

Using me as an example: Italy doesn’t charge state or local income taxes or property taxes. My monthly mortgage payment is under 1/10th of my combined writing and teaching income. And because I entered Italy at the right time, I secured a tax deal that puts my national income tax at an incredibly favorable rate. Unfortunately, last month, Italy closed the doors on many aspects of this deal.

However, many European, Asian, and Latin American countries still offer similar tax deals. Of course, as Americans, you’ll still have to file at home (usually), but that’s where your accountant comes in.

Sales tax (called VAT) is 22% and that sucks. But no country is perfect.

Because I eliminated the hefty costs usually taken as givens, I can now drink Starbucks all day. But since I get better coffee at an Italian gas station, I drink the local stuff instead.

Set aside a medical fund that you don’t touch for anything other than medical expenses.

This one mainly applies to those of you who wouldn’t even consider leaving the U.S.

According to a 2019 CNBC article:

A new study from academic researchers found that 66.5 percent of all bankruptcies were tied to medical issues —either because of high costs for care or time out of work. An estimated 530,000 families turn to bankruptcy each year because of medical issues and bills, the research found.

If you are 65 or older, you must set aside cash in a safe account. This will sound crazy, but if you’re in the States, I’d shoot for $100,000 in that account. That will cover most reasonable surgeries your insurance doesn’t.

Once my parents sold their house and came to Italy, their USD account that remained in the States serves this purpose. That’s why my mother gets the “side eye” from me whenever an Amazon package arrives for her. My look means, “That better have come from your social security check.”

Set aside a retirement fund.

You need a separate retirement account. This account should not be touched until you actually retire or have enough in it that a withdrawal beforehand won’t harm your ability to withdraw later.

Most people have barely enough for ten years of retirement. I want you to think bigger and healthier. Target a 25-year retirement. You’ll need to either save for it or invest enough in it that it works for you and grows itself.

How much will you need? That depends on your lifestyle.

The 4% Solution: only withdraw 4% per year from your retirement fund.

Here’s where my parents and their advisors made a catastrophic mistake: they withdrew too much every year.

If you withdraw 10% yearly without making any returns, you’ll deplete that account in 10 years. My father was 65 when they started withdrawing. He’s now 82. The math isn’t complicated: that account was empty long ago.

Why only 4%? Because in a 60/40 portfolio (60% equity, 40% bonds) the long-term return is 8.8%. That means your fund can still grow while you're in retirement. And you can leave a hefty inheritance to your children. It’s also conservative because markets can have bad years, too.

Let me show you:

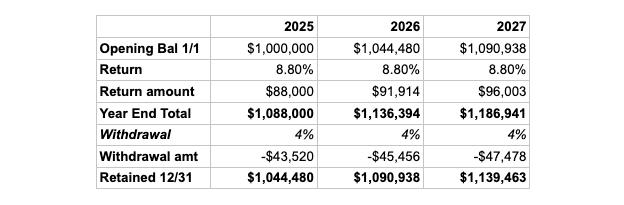

Let’s say you started with $1,000,000 in January this year. Then, you earned 8.8% over the next twelve months. That would give you a total of $1,088,000. On December 31, 2025, you withdrew 4%, or $43,520. That would leave you with $1,044,480 (1,088,000 - 43,520) to start January 2026.

You increased your retirement account while making a deduction from it.

You may think $43,520 isn’t enough for your lifestyle. Don’t forget to include any other Social Security or company pension payouts. For instance, my parents get about $3,200 monthly in Social Security payments. Those payments, combined with your personal account payout, give you $3,626 ($43,520 / 12) plus the $3,200, which equals $6,826.67.

That’s not bad if you’re living in the right place.

Wrap Up

If you haven’t taken any of these steps yet, don’t worry. Take action. Start today. Just thinking about these issues is a good start.

Then, move to making concrete plans to secure your future.

While Sherlock Holmes recommended a 7% solution (did you know he was a fictional cokehead?) a 4% retirement solution will go a long way.

The Market Nobody Ordered

Posted July 24, 2026

By Sean Ring

The Magic Pill’s Real Trick

Posted July 23, 2026

By Ray Blanco

Dead Cat Bounces

Posted July 22, 2026

By Sean Ring

Crude Lies

Posted July 21, 2026

By Matt Badiali

The SPR Boomerang

Posted July 20, 2026

By Zach Scheidt