Posted February 27, 2026

By Sean Ring

The Biggest RINO of Them All

My friend and Managing Editor of Paradigm Pressroom’s 5 Bullets, Dave Gonigam, wrote a fantastic piece yesterday titled, “Your Bank Wants Your Passport.” I would like to add my two cents to his excellent observations.

The whole thing riled me up, only because Americans will have to get used to what I’ve been used to since I left in 1999. Every time I open a bank account, it’s “Papers, please.”

I must produce my passport, Loss of U.S. citizenship certificate (because no foreign bank wants to deal with Yanks or their odious IRS), and ID card (yes, we already have them).

It’s not great, but it’s necessary when governments welcome immigrants willy-nilly. And the USG threw open the doors to the world during Joke Biden’s administration.

The problem is that citizens have to pay for their government's mistakes. (And thanks to The Donald’s most recent SOTU address, we know exactly how the Democrats feel about citizens.)

Tell me if this sounds familiar: If you like your bank account, you can keep your bank account.

Yes, you’ve heard that one before, concerning your doctor. It was a lie then, and in a different register, it’s a lie now.

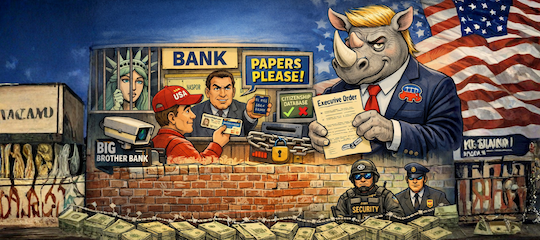

Because what Washington is quietly building under the patriotic banner of “border security” and “fighting terrorism” isn’t a wall at the Rio Grande. It’s a wall around you, and the mortar is your passport.

Borders Inside Banks

The Trump administration’s latest brainstorm is to force banks to verify everyone’s citizenship status. It’ll make your access to the financial system contingent on showing papers on demand.

The administration is selling this executive order (not legislation, I hasten to add) as a simple extension of “Know Your Customer” (KYC), which should be shortened to KY, if you know what I mean. It’s just a minor tweak to the post-9/11 compliance machinery. Banks already ask for ID, so what’s the big deal if they now must prove you’re a citizen?

Everything.

Because this isn’t about knowing who you are.

It’s about deciding what you are—citizen, foreigner, suspect—and then wiring that label directly into your ability to hold money, get paid, pay bills, or move capital.

You’re not just a customer anymore. You’re a status code.

Honestly, I don’t care about non-citizens. If you move to a country, you’ve got to follow the rules, whatever they are… and no, you don’t have the same rights as citizens. Sorry, not sorry. Deal with it, or leave.

But for citizens, this is a massive, invasive, and unnecessary headache.

From Hoppe’s Borders to Biden-Trump’s Bank Wall

Let’s bring in Hans-Hermann Hoppe for a minute. You don’t have to agree with his entire worldview, but he’s weirdly clarifying here.

Hoppe’s “ideal world” is a patchwork of private properties and covenant communities. Borders are just property lines. You move only by invitation: an employer hires you, a landlord rents to you, a road owner sells you access. No “public” commons, no welfare honey pot, no magical right to wander into someone else’s living room and then vote on their tax rate.

In that world, “border control” happens at the edge and at the door. Owners and their associations decide who they invite. If you’re inside, it’s because someone with skin in the game voluntarily took you in. If you misbehave, you’re ejected. That’s it. There’s no giant federal apparatus needed.

The point is immigration is handled where it should be—at entry and at association—not retroactively by strangling your access to money.

Now compare that to America 2026. It has a massive public-property sprawl: roads, schools, welfare offices, hospitals, and a 50-state patchwork of benefit rules. It also has a welfare-democracy where every migrant is also a potential client of the state and maybe a future voter. Finally, America has a security bureaucracy that hasn’t had a slow day since September 12, 2001.

External borders are political theater. Internal borders are where the real action is.

And the most powerful internal border of all is not a fence or a checkpoint. It’s your bank.

The Nationalization of Your Money

After 9/11, the financial system was deputized as a front line in the “War on Terror.” The Bank Secrecy Act, the Patriot Act, and anti-money laundering/know-your-customer (AML/KYC) rules… These were sold as temporary emergency measures to stop shadowy bad guys from wiring money to caves.

Fast-forward to the present. Every serious financial institution must collect extensive personal data, monitor your transactions, and report “suspicious” activity. Algorithms you’ll never see are scoring your behavior against risk models you’ll never read, feeding regulators you’ll never vote for.

And now, on top of all that, the state wants citizenship wired into the system.

No passport (or whatever document they anoint as proof)?

No compliant status?

Ok, then. Enjoy the cash-only life, comrade.

This isn’t a conservative policy. This isn’t a pro-market policy. This is a Western-style social credit system, dressed up in a MAGA hat.

At least the Chinese had the decency to be open about it.

“If you don’t control your external borders…”

Here’s the bitter punchline.

If a government refuses to control its external borders, but still wants to dictate who is “in” and “out,” it has only one choice.

It has to build internal borders.

These are chokepoints in systems the government cannot live without.

- Want to work? E-Verify.

- Want to travel? REAL ID at the airport.

- Want to bank? Show your passport, prove your citizenship, and pray the database likes you.

Each of these is an internal border check, where you must prove that you are the “right kind” of person to do something that used to be assumed: get paid, move around, hold property.

This is how you turn a country into a giant gated community patrolled by compliance officers behind terminals.

You don’t need to militarize the southern border if you’ve already militarized Citibank’s back office.

Why Hoppe Would Hate This

From a strict Hoppean perspective, this is exactly the wrong direction.

Yes, he believes in selective immigration based on property and association. But his borders are enforced by owners, not databases. Exclusion is at the point of invitation, not enforced by retrospectively shutting off your access to money. Communities can say “no” by not renting, not hiring, or not selling. Not by pulling your financial plug because you’re on the wrong side of a federal status flag.

What D.C. is building has nothing to do with property rights and everything to do with control.

In Hoppe’s ideal, if you’re not invited, you never get in. In D.C.’s new hoped-for reality, everyone gets in, and then the state sorts you through tax IDs, employment systems, landlord rules, and your bank accounts.

It’s the worst of both worlds: open enough to maximize chaos, controlled enough to maximize bureaucracy.

Money as Government Permission Slips

This is the real danger most people are missing.

Once the principle is accepted that access to the financial system is contingent on satisfying whatever status checks the federal government demands, the list of status checks can grow without limit.

Today, it may be “Prove citizenship.”

Tomorrow, it could be:

“Prove you’re not on this watchlist.”

“Prove you’re up-to-date on your tax filings.”

“Prove your social-media risk score is acceptable.”

“Prove you’re not a member of out-of-favor organizations.”

We aren’t there yet.

But DC is building the architecture, slowly and bureaucratically. KYC and AML gave the state the wires. Citizenship checks justify it. The next crisis will give it the excuse.

By then, arguing about walls and asylum quotas will look quaint.

What’s Next

I’m not going to pretend there’s an obvious solution. But there are lines that need to be drawn:

- No further expansion of status-based financial controls. Once you accept passports for bank accounts, you’ve conceded the key point, which is money (the residual of your income minus your expenses) is a permissioned privilege, not a property right.

- Attack the root problems like insane immigration law, bloated welfare, or endless war, rather than pretending you can paper over them with new database fields in bank compliance systems.

- Stop cheering when “your side” uses the financial system as a weapon. You won’t be the one holding the weapon forever.

If you really believe in controlled borders, then control your external borders. To Trump’s credit, he’s genuinely attempting to do that. But don’t compensate for a broken external policy by turning every bank branch into a mini-DHS field office and every citizen into a suspect who must periodically re-prove their right to exist financially.

Because once your bank balance depends on your papers being in order, you don’t live in a free country.

Wrap Up

When Candidate Trump first mentioned in 2016 that the Fed created a “false economy” and that George H.W. Bush made a huge mistake attacking Iraq, my faith in humanity was restored.

When President Trump started to show he was a Big Government conservative, I said that on any other timeline, The Donald would be a Kennedy Democrat.

Now, with this legislation and what seems to be an imminent war, I’m starting to think the biggest RINO of them all is sitting in the Oval Office.

At least Kamala isn’t President, right? Is that low bar all I have left to console myself?

Have a great weekend.

Models vs. Molecules

Posted April 17, 2026

By Jim Rickards

Watts Over Woke

Posted April 16, 2026

By Matt Badiali

The Woodpecker’s Tongue

Posted April 15, 2026

By Sean Ring

Autocrat Ousted; Congratulates Victorious Opponent

Posted April 14, 2026

By Sean Ring

The World’s Fragile Energy Tapestry

Posted April 13, 2026

By Sean Ring