Posted September 20, 2022

By Sean Ring

The 10-Year Yield Roofs It

Good morning from a glorious morning in Bodrum, Turkey.

I’m flying back to Italy via Istanbul early this afternoon. I miss my family, but I’ve had a wonderful time here.

Yesterday, we went on the famous PFS boat trip in the Mediterranean. After some seasickness, I recovered to have a great time with good food, wine, and company.

Some of the Property and Freedom Society speakers have promised me their speeches to reprint here in the Rude.

When I get them, you’ll be the first to know.

In the meantime, we’re finally seeing bond yields hike to more normal levels.

We’re not back to where I think we need to be yet, but we’re certainly moving in the right direction.

However, this will be a painful process… if the Fed has the cojones to stay the course.

In this edition of the Rude, I’ll look at the rise of the 10-year yield and what I think the repercussions are now.

Do You Yield?

Though Kevin Costner’s accent was slightly amiss in Robin Hood: Prince of Thieves, I still loved the film.

I was a junior in high school in 1991 when the movie came out.

I vividly remember the scene in the cold waters of an English river. There, Robin gets Little John to yield in their fight because John can’t swim and isn’t aware his feet could touch the bottom.

To yield is to give. In finance, it’s synonymous with “return.”

Fixed income traders and investors usually use the term “yield,” while equity traders and investors typically use the word “return.”

That’s because of the former compartmentalization of the markets. In the past, bond guys were bond guys. Equity guys were equity guys. That’s it.

But in our world, though that compartmentalization no longer exists, the different terms remain.

Concentrating on yields as rates, there are many different terms financiers use for it:

- The required rate of return

- The discount rate

- The cost of capital

- The internal rate of return

- The cost of carry

Project managers will use IRR to determine if a project is worth investing in. Investment bankers will discount their cashflows. Investors require a level of return to invest.

Rising yields simply mean investors, whoever they may be, demand more return in exchange for taking on a certain level of risk.

But the knock-on effect is this: if investors demand more return for their investment, asset prices will drop to accommodate their new investors.

And we see that across the board.

But first, let’s look at the 10-year yield itself:

We’re nearly at 3.50%.

I think we’re heading to at least 4.50%.

I’d love to see 5.00%.

But that will depend on whether Jay Powell stays his course.

If he backs down, we’ll see rate cuts next year.

But right now, the FOMC is petrified that inflation will run away from them.

I think it already has.

Let’s look at some other asset classes.

Gold

The problem with commodities is their cost of carry.

The cost of carry is the storage, insurance, and foregone interest (opportunity cost) of holding commodities.

But even if you don’t hold physical gold, your gold ETF will charge you the carrying costs.

So every time yield rises, your commodities will feel selling pressure.

I think gold is likelier to hit $1,500 than $2,000 right now.

Stocks and Crypto

Ah, competition. It’s something the stock market hasn’t seen for a long time.

And it shows.

But there’s a question every investor has to ask himself: if I can park my cash in bonds or a savings account for 4%, do I really need to be in the stock market?

I think the answer may surprise you.

Sure, with inflation at 8.5%, investors may still want to take on the extra risk to preserve more of their purchasing power.

But if the Fed successfully squashes inflation - a BIG if - there’s a sizeable portion of the investing population who’d happily keep more capital in cash.

As for crypto, from the beginning of 2020 to the end of 2021, Bitcoin was the only game in town.

That story changed markedly in 2022.

There are far more attractive income-returning investments to choose from than just crypto.

Bonds

The first thing you learn in Finance 101 is that bond prices are inversely related to their yields.

As bond yields increase, bond prices fall.

Treasury bonds have fallen out of bed, with the TLT down nearly a third this year alone.

Junk has fared better, but not much.

I see this trend continuing.

The inverse of the TLT, the TBT, has nearly doubled this past year.

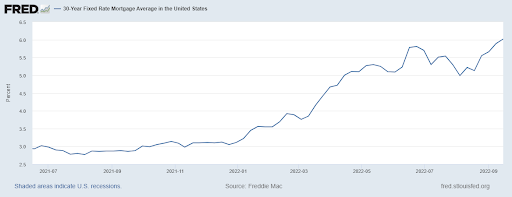

Housing

Straight from the horse’s mouth:

The above is a chart of the 30-year fixed rate mortgage average in the United States.

As of September 15th, the most recent reading, the rate is 6.05%.

That’s a bit tricky for most aspiring homeowners.

Especially for a generation of people who are used to near-zero rates.

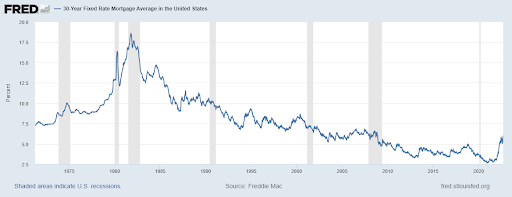

If we zoom out of the above chart, we see this:

That peak in the early 80s was when the Fed was under Paul Volcker, Jay Powell’s new spirit animal.

Mortgage rates reached 18.44% in late October 1981.

Imagine the pain of buying a house then!

Wrap Up

Jay Powell’s rate hiking cycle is wreaking havoc on asset markets.

Once the 10-yield peaks, we can start getting bullish.

But right now, it’s scary out there.

Yes, the market was up yesterday, but only a bit.

The day-to-day matters much less than the trend right now.

Ray’s Rockets!

Posted July 26, 2024

By Sean Ring

King: “It Can’t Happen Here”? Hey, It Just Happened Here!

Posted July 25, 2024

By Byron King

Nothing is Biden’s Fault

Posted July 24, 2024

By Sean Ring

The Democrats’ Dilemma

Posted July 23, 2024

By Sean Ring

Harris/Obama 2024?

Posted July 22, 2024

By Sean Ring