Posted July 19, 2021

By Sean Ring

Real Axes to Grind

Its Monday again.

Time to refuel with that first cup of joe.

Today, Im going to explain from another angle how the game is rigged and why the governments and banks never want the stock market to go down.

Its a function of how investment banks service asset managers, so theres no real solution to this issue. Im just calling out the positioning and the incentivization.

Types of Banks

First, let me list the types of banks. I just want to make sure were all on the same page.

Retail banks: these are banks whose primary business is deposits and loans. That is, they take in depositors money and then lend out a good size portion of it (nearly 90%) to borrowers in the form of mortgages, auto loans, and credit cards. Where normies bank.

Commercial banks: these are banks that service small to medium enterprises with overdrafts, lines of credit, and revolving loans.

Private banks: rich people have rich people problems. Besides fulfilling all the jobs of a retail bank, private banks also help with portfolio management, tax liability management, succession and estate planning, asset protection, and philanthropy.

Investment banks: these are banks that cater to large corporates, asset managers, and financial institutions. In the primary markets, they can do this by initial public offerings, mergers and acquisitions, and leveraged buyouts.

In the secondary markets, they facilitate trade for the buy-side (asset managers and hedge funds). Investment banks and brokerage firms make up the sell-side. The buy-side cant trade on exchange without the sell-side, as the sell-side banks and brokers are the exchange members.

Central banks: the Leviathan of our time. Responsible - their word, not mine - for monetary policy. They do this by controlling the level of interest rates in the economy. How? By conducting open market operations in the buying and selling of US treasury securities. Now, central banks buy other securities, such as agency securities, bonds, and stocks (Japan).

Now that thats sorted, were only going to deal with investment banks and their relationship to asset managers. The reason why is that the other types of banks dont do this business.

For the purpose of this piece, asset managers will include the obvious ones, such as BlackRock, the worlds largest with just over $9 trillion in assets under management (AUM), Vanguard, and Fidelity.

Well also include pension funds, sovereign wealth funds, insurance companies, and endowment funds, who either directly or through asset managers invest in the market long-term.

Heres the Issue

As Ive mentioned, investment banks service asset managers, or the buy-side. The buy-side is the people who take all of our assets and buy stuff, like stocks, bonds, commodities, and real estate.

Asset managers are buyers of mammoth amounts of stock. That means they are constantly long. Of course, if they're long, they always want the market to go up. And, yes, that is, for the most part, true.

But we must keep two things in mind, only one of which is obvious.

The obvious one is they don't want violent moves downward, such as the March 2020 Covid crash.

The not-as-obvious is they also don't tend to want the market to move too violently upwards, either.

Its like quality of earnings. A nice, steady increase is good enough for most of them. Of course, TSLA quadrupling is just fine and dandy. But asset managers wouldve certainly been at least partially hedged.

So asset managers do two things to combat a precipitous fall or to prepare for a sideways move in the stock. Here they are:

The Protective Put

An asset manager will go to their investment banks and say to them, "Listen, I'm long this stock that has, say, appreciated 40% in the past year. I need to hang on to it because it is a part of my investment plan, but I'm worried about the downside. Can I please buy a put from you?"

When you take a long stock position and combine it with a long put position, you have what's called portfolio protection. It synthetically creates a long call option on the stock.

That means you're still exposed to the upside, which is great, but you don't have any downside anymore. The asset manager eliminated that downside by paying the option premium.

The Covered Call

The second scenario is this: a fund manager may be forced to own a stock that is not particularly good - a dog, in asset management parlance - a stock that hasn't moved up in many years and doesn't pay the best dividend in the world.

But they have to hold it because it's a part of their index or basket. So what fund managers often do is sell call options against those stocks.

They are what we call covered call positions, and, synthetically, they are short puts.

The asset manager will do this for a few reasons:

- The asset manager immediately receives a premium from the sale of the put.

- That premium increases the managers return.

- The premium also acts as partial downside protection.

- Earning premium is better than paying out for a put when the asset manager doesnt expect a big fall in the stock price.

There is only one fundamental change that deflation brings about. It radically modifies the structure of ownership. Firms financed per credits go bankrupt because at the lower level of prices they can no longer pay back the credits they had incurred without anticipating the deflation. Private households with mortgages and other considerable debts to pay back go bankrupt, because with the decline of money prices their monetary income declines too whereas their debts remain at the nominal level. The very attempt to liquidate assets to pay back debt entails a further reduction of the value of those assets, thus making it even more difficult for them to come even with their creditors.

Yes, the games rigged. And in this particular instance, theres nothing we can do about it.Have a great start to your week!All the best,Sean

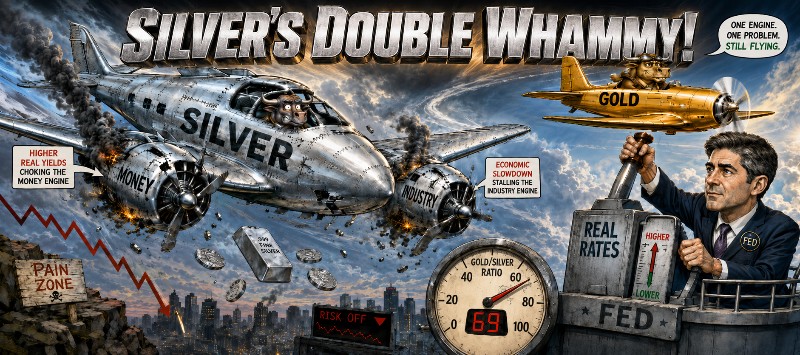

The Market Nobody Ordered

Posted July 24, 2026

By Sean Ring

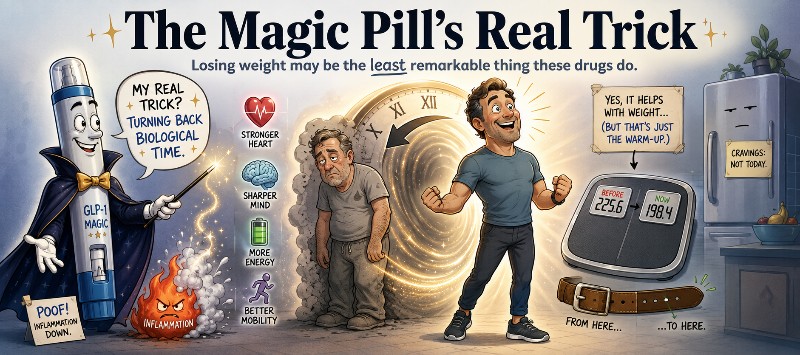

The Magic Pill’s Real Trick

Posted July 23, 2026

By Ray Blanco

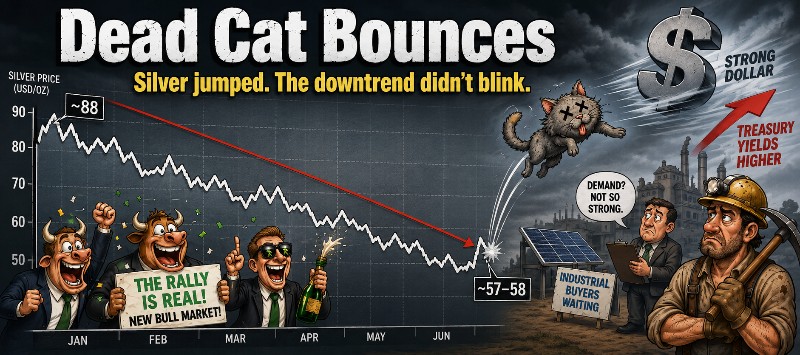

Dead Cat Bounces

Posted July 22, 2026

By Sean Ring

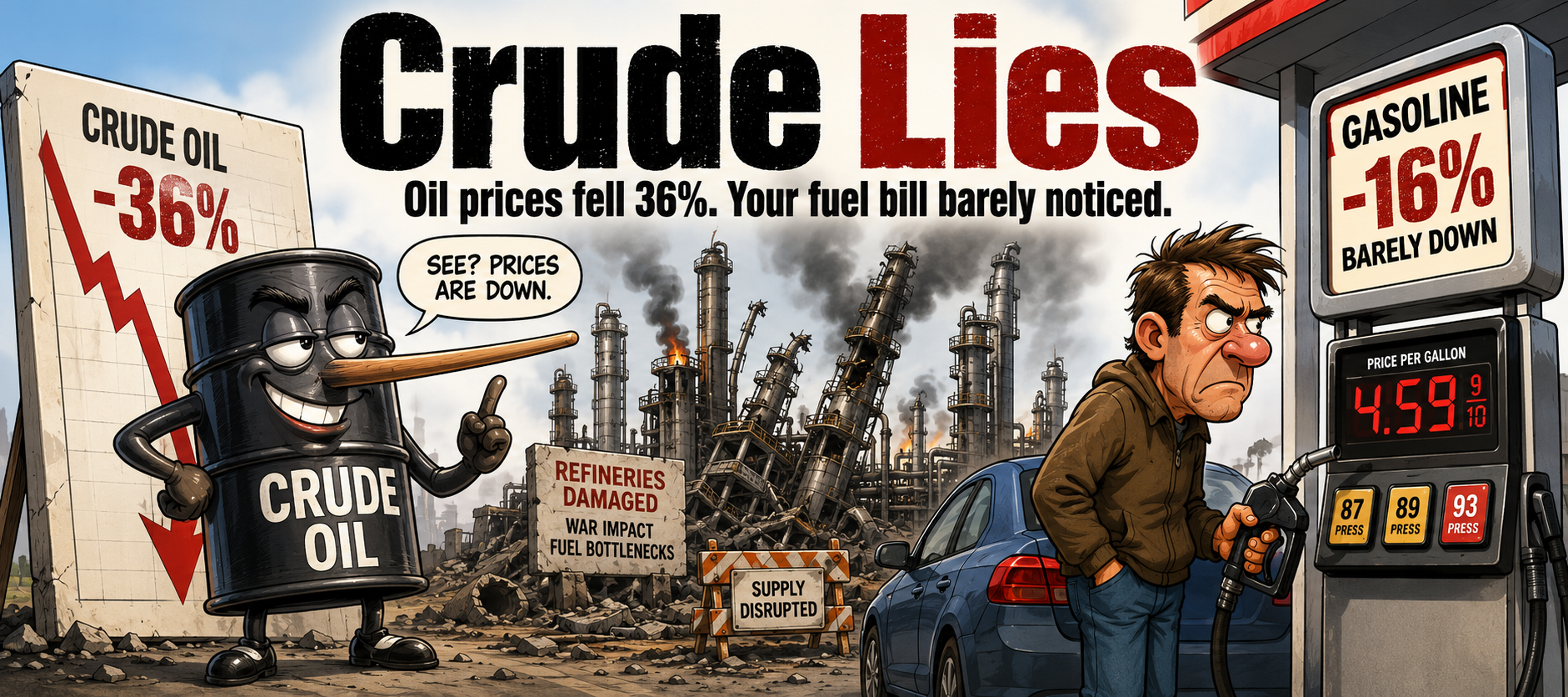

Crude Lies

Posted July 21, 2026

By Matt Badiali

The SPR Boomerang

Posted July 20, 2026

By Zach Scheidt