Posted April 01, 2026

By Sean Ring

No Quarter in March

Welcome to this month's brand-new asset class review that walks through every major market from equities to crypto, chart by chart, number by number. The goal is simple: cut through the noise, look at what the price action is actually telling us, and give you a clear-eyed read on where each market stands as we head into a new month.

Markets are complex, but they aren’t random. Every chart in this report tells a story — about momentum, about sentiment, about the tug-of-war between buyers and sellers. The moving averages we use (10-week and 40-week, roughly equivalent to the 50-day and 200-day) are our primary trend filters. When the price is above both, the trend is with you. When it's below both, it isn't. Everything else is commentary. Please note that “cautiously bullish” or “cautiously bearish” is when the price is between the moving averages.

We cover fifteen assets across eight categories: US equities, rates, the dollar, bonds, real estate, energy, metals, and crypto. Each gets a chart, a stats table, and a short commentary. At the end, you'll find summary return tables across traditional assets and crypto, ranked by month-to-date performance.

As always, the commentary is a starting point for your own thinking, not a substitute for it. Let’s get to it.

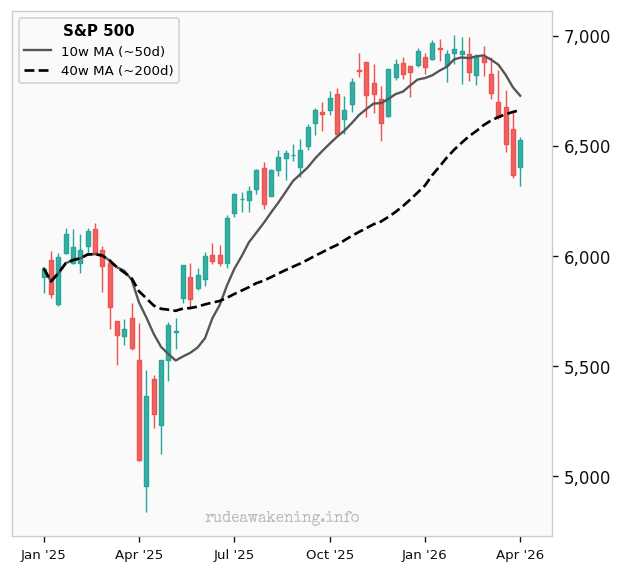

S&P 500

Commentary

The S&P 500 has broken below both its 10-week MA (6,793.92) and 40-week MA (6,638.86), confirming a bearish trend. Breadth has deteriorated, with defensive sectors outperforming cyclicals as the Iran situation and its impending expected inflation weigh on risk appetite. A relief rally is possible near term, but the burden of proof is on the bulls to reclaim the 40-week MA before this can be called anything more than a bounce.

Target / Risk

Nasdaq Composite

Commentary

The Nasdaq Composite sits below both its 10-week and 40-week MAs and is in a bearish trend. Mega-cap technology names that drove the 2025 rally have been the biggest drag, with multiple compressions hitting hardest where valuations were most stretched. The AI trade is undergoing a reality check after two years of outsized gains.

Target / Risk

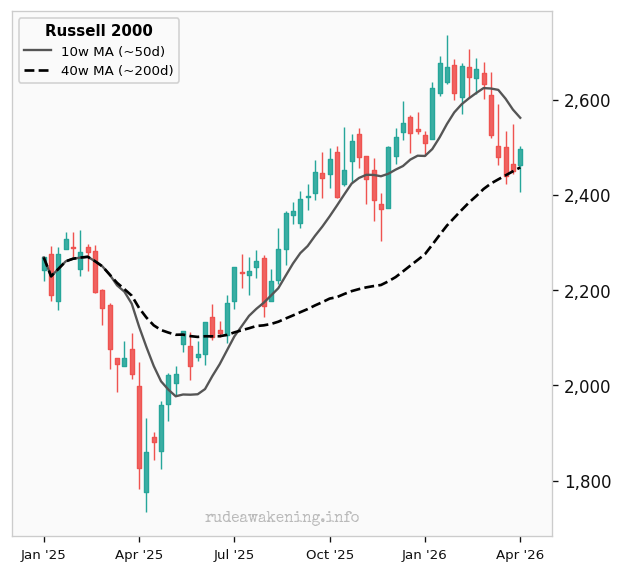

Russell 2000

Commentary

The Russell 2000 is clinging to its 40-week MA (2,441.32) despite pressure, with the 10-week MA (2,595.44) already lost. Small caps are more domestically oriented, offering some insulation from trade war fears, but they are also more exposed to tighter credit conditions and a weakening, debt-laden consumer. A sustained break below the 40-week MA would confirm broader market deterioration.

Target / Risk

The Russell still clings to a 3,213 upside target, but I don’t think that’s within reach now.

US 10-Year Yield

Commentary

The bond market is pricing in persistent inflation and fiscal concerns, with the term premium rising as foreign buyers reduce their appetite for US Treasuries. This creates the uncomfortable stagflation signal: stocks and bonds falling together. The 10-week average sits at 4.20% and the 40-week at 4.19%; watch 4.5% as the key resistance. A sustained break above it would put serious pressure on equity valuations.

Target / Risk

4.96% is the next upside target.

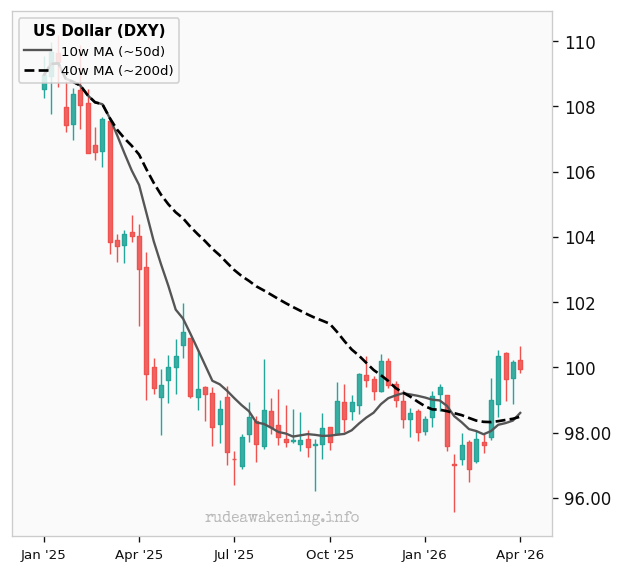

US Dollar (DXY)

Commentary

The US Dollar Index’s trend is currently bullish. The longer-term backdrop remains dollar-bearish as twin-deficit concerns intensify and foreign investors quietly reduce their US exposure. A sustained break above the 40-week MA would challenge the bear case; a break below 99 would signal a meaningful resumption of the downtrend.

Target / Risk

The downside target of 79.76 looks in jeopardy.

TLT (20Y Bond)

Commentary

Long-duration bonds continue to bear the brunt of the yield rise. The risk here is a vicious cycle: rising yields tighten financial conditions, weakening growth… but if the market doubts the Fed's resolve, bonds can sell off alongside stocks. The 40-week MA at 86.84 is the key level to reclaim for any durable recovery.

Target / Risk

No clear targets for TLT.

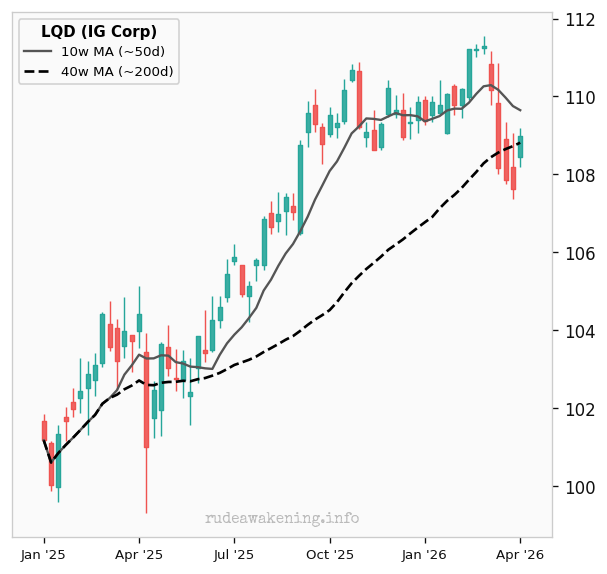

LQD (IG Corp)

Commentary

Investment-grade corporate bonds are cautiously bullish, sitting near both the 10-week MA (109.90) and 40-week MA (108.64). Credit spreads have widened modestly as growth fears build, though the move has been orderly. Markets aren’t yet pricing in a recession. The key risk is forced selling if equity volatility spikes; anything above 120bps over Treasuries would signal growing stress.

Target / Risk

No clear targets on LQD.

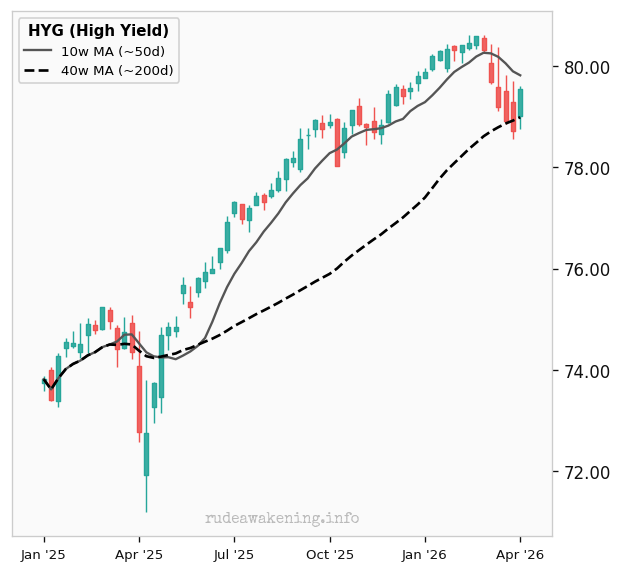

HYG (High Yield)

Commentary

High-yield has held up somewhat better than investment-grade on a relative basis, reflecting the shorter duration profile of junk bonds. Spreads have widened but not dramatically. Credit markets aren’t pricing in a default cycle… yet. A deterioration in the jobs market could see spreads blow out quickly.

Target / Risk

No clear targets on the HYG.

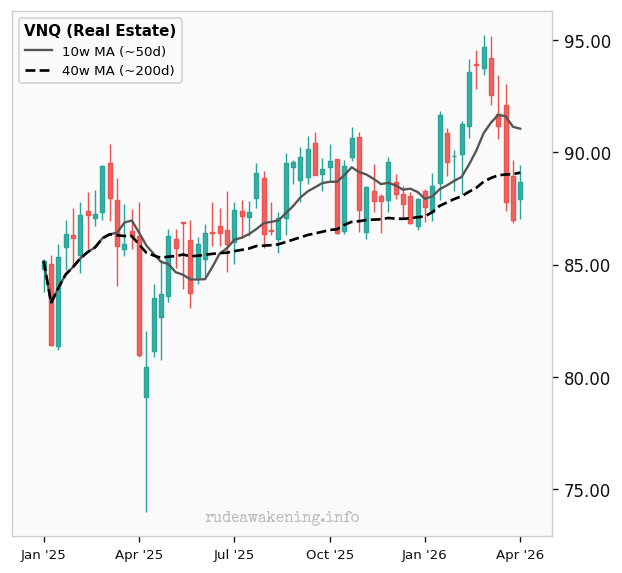

VNQ (Real Estate)

Commentary

Real estate is bearish, with VNQ below both MAs — 10-week at 91.23, 40-week at 88.89. Higher long-term yields are squeezing cap rates and making the dividend yield less attractive relative to risk-free alternatives. Office remains structurally challenged post-pandemic, and residential REITs face affordability headwinds. Unless the 10-year yield pulls back meaningfully, the near-term bull case is limited.

Target / Risk

No targets on the VNQ.

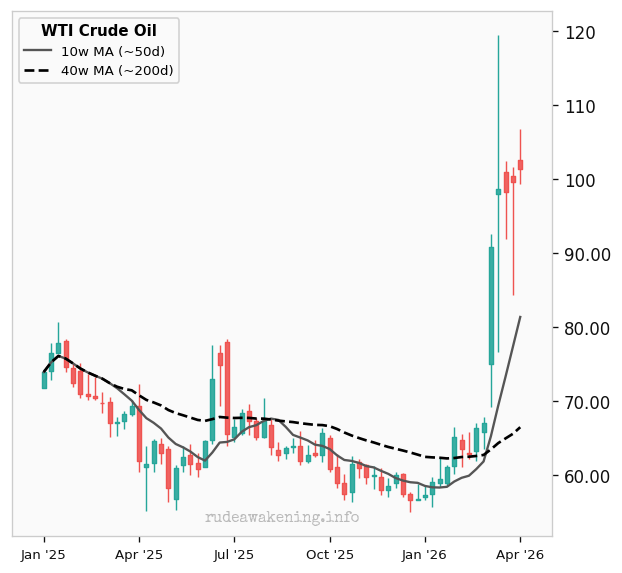

WTI Crude Oil

Commentary

OPEC+ discipline and geopolitical risk premiums (read: war) put a bid under crude, though demand concerns tied to a slowing global economy are capping upside. The supply-demand balance remains tighter than consensus expected.

Target / Risk

No targets, but if this war keeps up longer, we’ll see $150 per barrel or more.

Copper

Commentary

Copper has been reassessing the pace of the global manufacturing recovery, with China's property sector remaining a structural drag despite stimulus measures. The long-term electrification and energy transition story keeps a floor under prices. The physical market is genuinely tight. 5.24 is the key level; a break there would signal a more meaningful growth slowdown.

Target / Risk

An upside target of 5.90 and a downside target of 5.24.

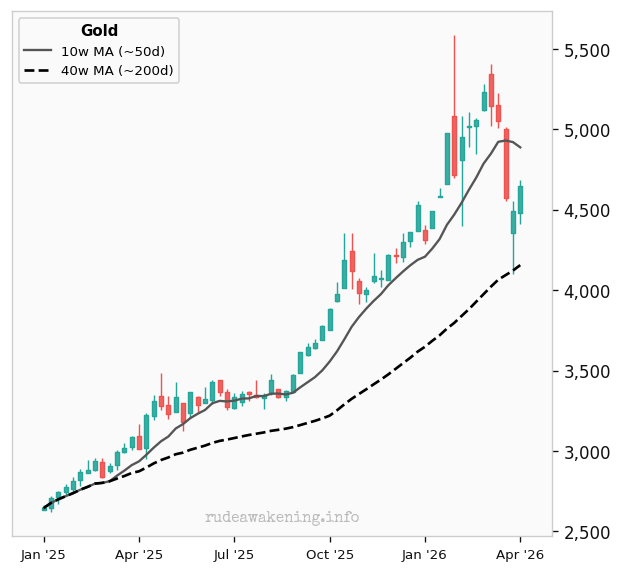

Gold

Commentary

Gold has been among the standout performers of 2026, driven by central bank buying, dollar weakness, and its role as a hedge against both inflation and geopolitical risk. The yellow metal has decoupled from its traditional inverse relationship with real yields — a structural shift worth watching.

Target / Risk

No upside targets yet.

Silver

Commentary

Silver has lagged gold, as the industrial demand component — roughly half of total demand — faces pressure from a slowing global manufacturing cycle. The gold/silver ratio has widened, historically a sign of risk-off conditions. When the cycle turns, silver tends to outperform gold sharply to the upside — patient bulls may be rewarded, but timing is everything.

Target / Risk

A 64.05 downside target remains.

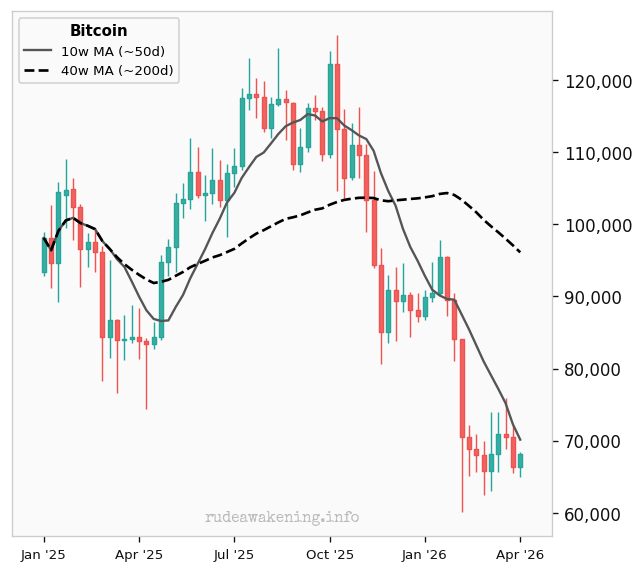

Bitcoin

Commentary

Bitcoin has shown some resilience relative to equities, a modest decoupling that crypto bulls will point to as evidence of maturing as an asset class. The 40-week MA at 90,589 remains the medium-term trend line to reclaim; a sustained break above it would shift the technical picture meaningfully positive.

Target / Risk

Meaningful downside targets of 56,250 and 55,420.

Ethereum

Commentary

Ethereum has been the weaker of the two major cryptos, with the ETH/BTC ratio in a persistent downtrend as Bitcoin dominance rises in risk-off environments. The 40-week MA at 3,055.67 is well above current prices. A recovery above the 10-week MA would be the first sign that sellers are exhausted.

Target / Risk

ETH still has $1,590 as a downside target.

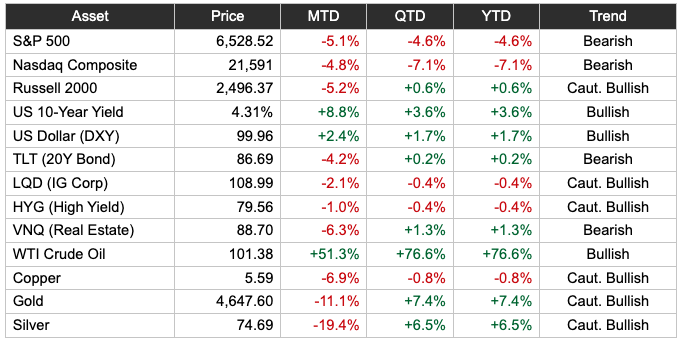

Summary: Traditional Asset Classes

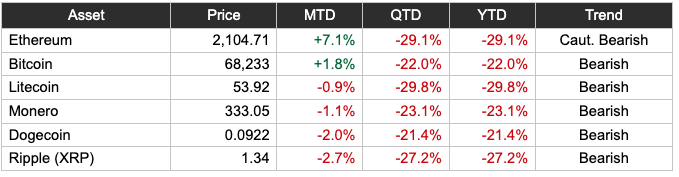

Summary: Crypto

Wrap Up

Every month has its own character, and this one is no different. Some assets are trending cleanly; others are chopping around their moving averages, looking for direction. The summary tables at the end of this report tell the month-to-date story in one place — who won, who lost, and by how much.

The most important thing you can take from this report is not any individual commentary, but the overall picture.

Stay nimble, keep your stops tight, and remember: in uncertain environments, cash is a position too.

Black Box State

Posted June 23, 2026

By Sean Ring

Financial Fathers

Posted June 19, 2026

By Sean Ring

The Fed's Cold Turkey

Posted June 18, 2026

By Sean Ring

Hormuz Premium

Posted June 17, 2026

By Sean Ring

Wuhan Whoopsie!

Posted June 16, 2026

By Sean Ring