Posted May 16, 2025

By Sean Ring

How to Retire Without Running Out—or Running Scared

I take off for Riyadh tonight, so I thought I’d go through the mailbag this Friday morning. Thank you for taking the time to write in. It’s always great to read your thoughts. However, I’m only answering one piece of mail today, as it’s about the critical issue of retirement.

I’ll get straight to it.

Retirement Numbers

I agree numeracy is important because it adds quantification and weighing to logic. However, the apparent precision can be more deceitful for much the same causes -- false or missing facts. …

Oh, as I wrote originally, your Net Worth equation appears to assume a savings rate of 10% without correction for education or income progression. As such, I see it as an aspirational sales-tool for personal financial anal-ists peddling their paper. As Mark Twain wrote: "Figures don't lie, but liars figure." Because both persuade.

Robert R.

Robert, I’ve been thinking about this since you first wrote in about it. I’ll address it now.

First, for clarity, let me reprint the net worth equation so we’re on the same page. (Bolds mine.)

“Net Worth Indicator

This is a great targeting mechanism, and I regrettably only just found it. It’s from The Millionaire Next Door by Thomas J. Stanley and William D. Danko.

Multiply your age times your realized pretax annual household income from all sources except inheritances. Divide by ten. This, less any inherited wealth, is what your net worth should be.

If you hit this number, you’re an AAW or average accumulator of wealth.

According to the authors, to be considered a PAW, or prodigious accumulator of wealth, you “should” have at least twice this number.

What I like about this indicator is that it’s simple to calculate and gives you a target.

Full disclosure: I’m a UAW, which means I’m an under-accumulator of wealth.

But I won’t use this number to feel bad. I choose to think bigger and get better results.

If you’re unhappy with what this number tells you, I suggest you do the same.

Julian H. wrote in with this great question about the formula:

I'm familiar with The Millionaire Next Door book and have always wondered what the logic behind the formula age x income / 10 is. Do you have any knowledge about that? There are no specifications in the book, and I can't find anything valuable on the Internet.

Thanks in advance.

Best.

Julian H.

Julian, as far as I can see, this formula is produced with linear regression. The authors took net worth, age, and income and produced a line of best fit.”

Second, as you can see, there aren’t any assumptions: the formula is merely an equation for a linear regression that produces the best fit.

Third, I like this formula because it initially made me think much bigger than I was thinking. The number that the regression equation produced was larger than I thought I needed for a good retirement. Since most people underestimate what they spend and how long they’ll live, this is a good thing.

However, to your point, I now realize the number the formula produces for me is too small!

I’ve been thinking about this a lot, so I wrote this on April 8th:

“The 4% Solution: only withdraw 4% per year from your retirement fund.

Here’s where my parents and their advisors made a catastrophic mistake: they withdrew too much every year.

If you withdraw 10% yearly without making any returns, you’ll deplete that account in 10 years. My father was 65 when they started withdrawing. He’s now 82. The math isn’t complicated: that account was empty long ago.

Why only 4%? Because in a 60/40 portfolio (60% equity, 40% bonds), the long-term return is 8.8%. That means your fund can still grow while you're in retirement. And you can leave a hefty inheritance to your children. It’s also conservative because markets can have bad years, too.

Let me show you:

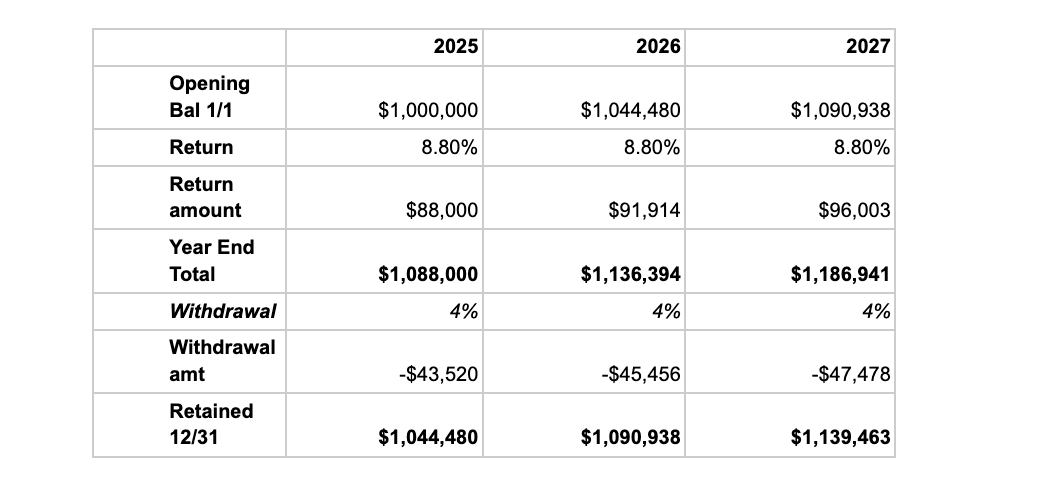

Let’s say you started with $1,000,000 in January this year. Then, you earned 8.8% over the next twelve months. That would give you a total of $1,088,000. On December 31, 2025, you withdrew 4%, or $43,520. That would leave you with $1,044,480 (1,088,000 - 43,520) to start January 2026.

You increased your retirement account while making a deduction from it.

You may think $43,520 isn’t enough for your lifestyle. Don’t forget to include any other Social Security or company pension payouts. For instance, my parents get about $3,200 monthly in Social Security payments. Those payments, combined with your personal account payout, give you $3,626 ($43,520 / 12) plus the $3,200, which equals $6,826.67.

That’s not bad if you’re living in the right place.”

Where to Start?

The trick is arriving at that first number… What do you need in your account at the start of your retirement? A simple way to find out is to take what you’d like to spend annually and divide it by 4%.

For instance, if your house is paid off, your children are no longer dependent on you, and you live in a cheap part of the world, you may settle on $40,000. $40,000 / 4% = $1,000,000.

If you’re used to a more lavish lifestyle, you may want to be able to spend $250,000 per year. $250,000 / 4% = $6,250,000.

You can have a wealthy, fulfilling retirement, and then, once you’ve shuffled off your mortal coil, you can leave a nice estate for your children.

Of course, you can adjust the numbers accordingly.

For example, let’s say a 50-year-old makes $100,000 per year. Using The Millionaire Next Door formula, his net worth should be $500,000. However, using the 4% Solution only gives an annual payout of $20,000. That’s only $1,667 per month. Even adding in Social Security payments probably won’t give him enough.

So he needs to adjust his expectations and earning power. If he wants to spend the $100,000 per year he currently makes in retirement, he’ll need $2,500,000 to start. He’s got time to get to $2,500,000, though it’ll be a long road. Perhaps $50,000 will do. That’s $1,250,000 he’ll need to save.

Wrap Up

Robert, I hope this makes you rest easier. Of course, everyone’s circumstances are different, and your mileage will vary.

But just thinking about the numbers, however you do it, is a great place to start. Retirement is too important to be left to the politicians currently plundering your Social Security fund.

Have a wonderful weekend!

Beware the Ides of May

Posted May 15, 2025

By Sean Ring

Trump’s Riyadh Revival: Peace Through Power—and Profit

Posted May 14, 2025

By Sean Ring

Oil, Guns, and Freedom: Alberta’s American Dream

Posted May 13, 2025

By Sean Ring

GREEN NEW SCAM: Biden’s $93 Billion Crony Climate Heist

Posted May 12, 2025

By Sean Ring

❤️🔥HOLY SMOKE! An American Pope!

Posted May 09, 2025

By Sean Ring