Posted June 19, 2026

By Sean Ring

Financial Fathers

Welcome to a Rude Double Edition on this fine Juneteenth!

Every Wednesday, the editors at Paradigm Press get on a call to argue about markets, macro, and the occasional geopolitical mess.

On Wednesday, our sharp-edged markets editor, Enrique Abeyta, threw a different question at the group.

His son Kai just turned 13. His daughters are heading to France with their mother for four weeks, so Enrique has his boy all to himself. He decided to turn it into a financial boot camp.

So he asked the room: if you had one piece of financial advice to give a 13-year-old, what would it be?

What came out of the next 45 minutes was one of the best editorial meetings we've had. Not because we covered markets, but because we covered what matters.

Twelve of us shared what we'd tell a kid. Here's all of it, sorted by contributor, in their own words.

Enrique Abeyta: Show Them the Numbers

Enrique's first lesson for Kai was compounding, not as a concept, but as a spreadsheet exercise.

He built a simple model: $1,000 invested for 50 years at 1%, 2%, 5%, and 15%. Then he added a second variable — what if you also contributed $100 every week? Two compounders working at once: return and consistency.

"The numbers are mind-blowing," Enrique said. "$1,000 turns into $8,000 in one scenario and $725,000 in another. He got it. It sunk in."

His point was simple: a 13-year-old has something no one on that call has. He has 50 years. Maybe 60 or 70. At those timelines, the math does all the selling for you.

Enrique also mentioned paying for grades — $100 per A, with a $250 bonus for a clean sweep across five classes. His logic: would he pay a tutor $750 to guarantee all A's? Without hesitation. So why not pay the kid directly?

Aaron Gentzler: Start Today. Not Tomorrow. Today.

Aaron's advice is the oldest line in investing, said without apology.

"The best time was the day you were born. The second best time is right now. We're going online, we're opening an account, and we're putting 500 bucks in it."

His 7-year-old daughter already has accounts. They talk in terms of buckets and pies — this pile goes away for a rainy day, that one stays ready.

Simple. No excuses. Start today.

Byron King: Get Paid for Being Useful

Byron's advice cuts to the bone. Learn how to do something. Then charge for it.

When his daughter Beatrice was 10, she asked what she could do. They had cats. Other people had cats. Other people went on vacation. So Beatrice started Beatrice's Cat Sitting Service. By high school, she had 7 or 8 regular clients and went off to college with money in her pocket.

Byron's point is not just financial. It's about building the mindset that your skills have market value and that you can find out exactly what that value is by offering them.

You don't need to be a coder or a rocket engineer. Mow lawns. Walk dogs. Know how to drive a nail. Get paid for being useful.

Scott Sutton: Build the System Early

Scott has two kids, ages 7 and 8. He uses a wall screen called Skylight that assigns tasks with star values. Clean the living room: two stars. Clean the toilet: five stars. Each star equals a quarter.

The twist: the stars can be redeemed for cash, but the payout structure rewards patience. Save up to 100 stars, and you don't get $50 — you get $75. The more you save, the higher the conversion rate.

He added one parenting trick that impressed the room: when one kid does something right, he rewards both kids and has the second one thank the first. The lesson sticks twice.

Mohan: Discipline, Then Asymmetry

Mohan started with a life lesson, not a financial one. Both parents need to be aligned. Kids are expert negotiators. If mom and dad aren't on the same page, the lesson doesn't land.

His financial point was elegant. Say a kid earns $10 mowing a lawn. You can't expect a 13-year-old to save all of it. So tell them to save just $2. Keep $8 if you want. But that $2 goes into two separate buckets.

One dollar into a broad stock index at an 8-10% annual return. One dollar into Bitcoin, at a hypothetical 15% annual return. Both compounding from age 13.

The index grows steadily. The crypto bet might go nowhere — or might go 100-fold. One is safe. One is a risk. Teach them the difference early, and let them feel it.

Mohan also shared a visual for compounding that beats any spreadsheet: an ancient Indian fable about a chessboard. Put one grain of rice on the first square. Double it on each subsequent square. By the 64th square, all the rice in the world isn't enough to fill it.

Zach Scheidt: Price Is What You Pay, Value Is What You Get

Zach's lesson builds on compounding, but adds a caveat most people never hear.

How much you pay for something matters. A great company at the wrong price is a bad investment. Tesla at 200 times earnings might be a great car, but it's a punishing entry point. The dot-com stocks were real companies. The problem was what people paid for them.

The Peter Lynch maxim — "buy what you know" — is dangerous without the second half: buy what you know… at a fair price. Shake Shack makes excellent hamburgers. It was not an excellent stock at 100 times earnings.

Popular stocks are usually priced for perfection. When the froth comes out — and it always does — the people who paid anything for something great get hurt the worst.

Dan Amoss: Learn from the Greats, Then Find Your Temperament

Dan pointed to something the others left out: timeless investment principles exist, and someone already figured them out.

Start with Warren Buffett's lineage. He learned quantitative cigar-butt investing from Ben Graham. Then Charlie Munger pushed him toward quality businesses — companies that delight customers and keep them coming back without needing heavy reinvestment.

Costco is Dan's case study. It always looked expensive. But it compounded capital so fast and left so much value on the table for customers that it kept printing returns. That's a model, not a fluke.

On the other side, Dan offered a contrarian test: look up the most popular, highest-market-cap stock every decade. It's always something different. The Nifty 50 in the 1970s. Japan in 1989. Dot-coms in 1999. Banks in 2007. What's most hyped usually ends in poor returns.

His final point: find what works for your temperament. We're not all the same. The best approach is the one you'll actually stick with.

Erik Kestler and Armando Gayleard: Don't Gamble. The House Always Wins.

This one landed hard. Erik Kestler said it plainly: the most important thing you can tell a 13-year-old boy today is don't gamble.

Online sports betting is hitting young men from every direction. Celebrity endorsements. Polymarket ads. Every influencer they follow. Armando confirmed it — every one of his little brother's friends is doing sports betting, and every celebrity they watch is pushing it.

Enrique connected it to something deeper. Gen Z feels locked out of the system. When kids believe the game is rigged against them, a 13-leg parlay starts to look like a retirement plan. Teaching a kid that they can actually build wealth — through work, through compounding, through patience — is the antidote to fatalism.

Mohan added that NIH research links online gambling to sharply rising suicide rates among young men. Gambling is a predatory industry targeting young men who don't yet understand odds.

Chris Campbell: Understand Risk — and Find Your Mentors

Chris came to this meeting at the right moment. Two weeks earlier, he'd reunited with a long-lost younger brother.

Chris's two lessons for him — and for any young person — were these.

First: understand risk. The riskiest thing you can do is sometimes nothing. Standing still. Staying comfortable. For his brother, that's the biggest danger.

Second, find the highest-density group of mentors you can. At 23, Chris read a book by Bill Bonner, tracked down his company Agora, and moved to Baltimore with $2,000 saved. He got the job. He got the mentors. Many of them were on this call.

As Enrique put it, that's courage. Moving to Baltimore. That's the real thing.

Matt Insley: The Barbell — Be Prudent First, Then Aggressive Later

Matt's advice came in two stages by age.

From 13 to 25: be prudent. Save money. Don't do stupid things. Learn discipline. Build the foundation.

After 25: learn the game of money. The people who got wealthy often didn't just save. They took the barbell approach — safe money on one side, aggressive bets on the other. Some started businesses and failed. Some went into debt for real estate and made it. The prudent-only path doesn't always win against people who took calculated risks.

His second point was more important. Social currency matters more than financial currency. The right friends, the right mentors, the right network — those compound too. Find people who are good and trustworthy, and build genuine relationships with them.

Doug Hill: Dollar-Cost Average and Don't Miss

Doug's grandfather was a doctor who survived World War II. His advice was simple: save 10% of every paycheck.

Doug's update: dollar-cost averaging. Put a small amount in regularly and don't stop. His son started at 24, putting a dollar a day across 15 to 20 assets on Robinhood. By 30, he had $60,000 — money that never felt missed because it was gone before he could spend it.

Doug's teaching trick: ask a kid, "Would you rather have $1 million right now, or a penny that doubles every day for a month?" They'll take the million. Then show them what the penny becomes. That exercise does more in five minutes than any lecture.

By the 31st day, the penny is worth over $10 million.

Adam Sharp: College Isn’t the Only Path

Adam Sharp backed up the anti-gambling point first — a 13-leg parlay is not a retirement plan, and kids need to hear that directly.

But his main point was bigger. You don't have to go to college.

His son is starting an apprenticeship as an electrician next year — his senior year of high school. It's an 8,000-hour, four-year program. He gets paid the entire time instead of paying tuition.

Supply and demand: there are too many college graduates and not enough skilled tradespeople. AI is going to displace a lot of white-collar work over the next 50 years. Electricians, plumbers, and mechanics are harder to automate. The pay gap is already closing. In many places, it's already reversed.

Let kids know there are respectable, well-paying alternatives to four years of debt.

Armando Gayleard: Work for What You Want

When Armando was 11 or 12, he wanted his own guitar. His father wouldn't buy it.

Instead, his father took him to the local recreation council and helped him ask for a job — lining baseball fields, cutting grass, whatever they needed. Two months later, Armando had $150. He walked into a music store and bought his first guitar.

"Something clicked in my head," he said. "If I want stuff, I can work for it and then go get it."

He now has a studio full of guitars and makes money with them.

His father also had a habit of saying, when Armando wanted to learn something neither of them knew how to do: "I don't know, but we can learn." That phrase, Armando said, gave him a belief he still carries: no task is insurmountable. You just spend the time.

James Welch: Show Them What a Dollar Buys

James has two kids, ages 4 and 7. After starting a chores system for quarters, he took them to 7-Eleven with a dollar each.

His daughter came back with a pack of balloons that burst when you tried to blow them up. His son found out a ring pop was $1.30 and had to be spotted 30 cents by his father.

It landed. His daughter is now saving for a $16 tub of slime. She knows what it costs in chores. She knows how long it'll take.

James's point: before you teach compounding and dollar-cost averaging, teach a kid what money actually buys. Prices go up. They never go down. That's not an inflation lecture — it's a field trip to the convenience store.

Sean Ring: 1% Better Every Day, and Read Everything

My contribution came in three parts.

First, show kids the compounding spreadsheet — but instead of money, use skill improvement. If you get 1% better at something every day for a year, you end up 37 times better than when you started. That number hits hard.

Second, when you're setting yourself a challenge, take 4% steps. Big enough to stretch you and create productive stress — what psychologists call eustress — but not so big it breaks you.

Third, learn to love the plateaus. I read a book called Mastery by George Leonard, an Aikido master. His core insight: learning is a staircase. You plateau, consolidate, then leap forward. Most people quit right at the plateau — right before the jump. If you know you're on a plateau, you keep going. The leap will come. (You can read the full article on this here.)

At home, my son Micah is obsessed with World War II battleships. He just finished the LEGO models of the USS Missouri and the Bismarck. He asked for the Yamato next. I said yes — in exchange for reading a book and giving me a chapter-by-chapter summary.

Which leads to the last thing: read. Voraciously. Nobody does it anymore. It will give them a comparative advantage that is almost impossible to overstate.

Alan Knuckman: Optimism Wins

Alan closed the session, and he kept it tight.

His daughter earned her way into a selective enrollment high school in Chicago, saving the family roughly $50,000. His advice to her: if you finish college in three years instead of four, the fourth year's tuition is yours. Real money. Real incentive.

But his biggest lesson was the mindset: optimism wins.

Young people today are surrounded by a narrative that the world is against them, that they can't make it, that the system is rigged beyond repair. Alan pushed back on all of it. The world has always been hard. Every generation faced something. The ones who made it were not the ones who gave up. They were the ones who believed opportunities were real and went after them.

"The only thing stopping you is you," he said. "That's what we have to communicate to kids."

Wrap Up

16 men and 16 lessons. All of those things schools have refused to teach for decades.

Here's the list, stripped to the bone:

Start investing now. Not next year. Now.

Show them the compounding spreadsheet. Make them feel the numbers.

Pay for good grades.

Teach them to earn money by being useful.

Build reward systems that make patience pay more.

Don't gamble.

Don't confuse popularity with value.

Learn from the greats, then find your temperament.

Understand risk — including the risk of standing still.

Find mentors and go where the money is.

Be prudent early, then take calculated risks later.

Dollar-cost average and don't stop.

Consider the trades over college debt.

Work for what you want.

Show them what a dollar buys.

Take 1% steps every day. Love the plateau. Read everything.

Optimism wins.

None of this is on the SAT. None of it is in the curriculum. The people who benefit from financial confusion have made sure of that.

You now have the whole list. Pass it along.

The Last Great Crack

Posted July 28, 2026

By Matt Badiali

The Consent Nobody Gave

Posted July 27, 2026

By Sean Ring

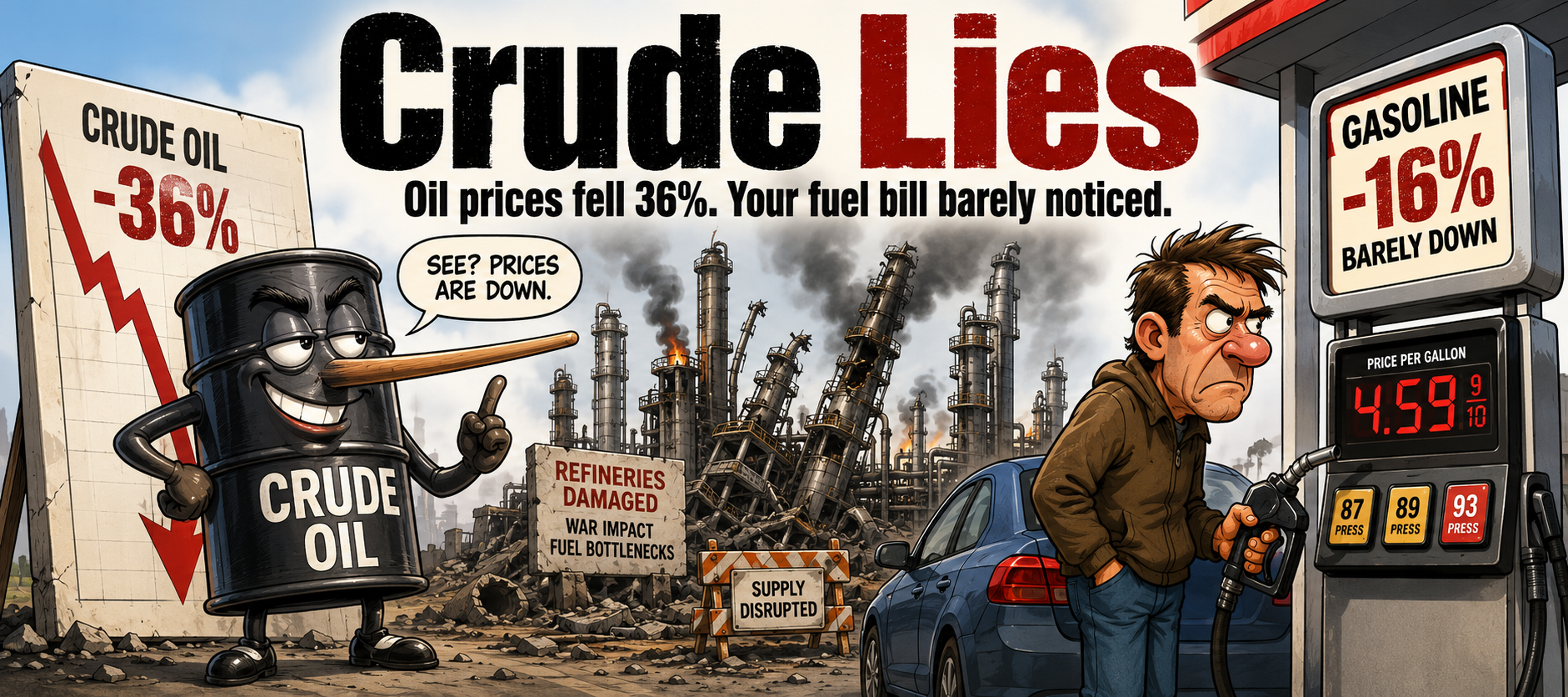

The Market Nobody Ordered

Posted July 24, 2026

By Sean Ring

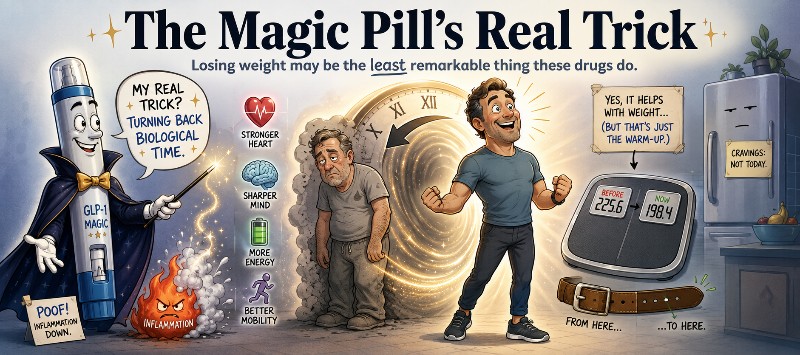

The Magic Pill’s Real Trick

Posted July 23, 2026

By Ray Blanco

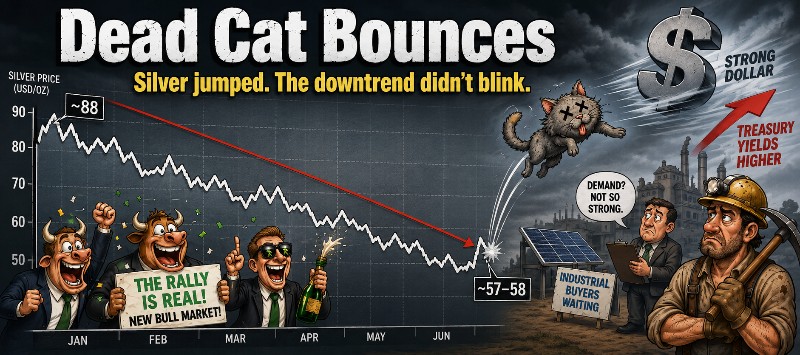

Dead Cat Bounces

Posted July 22, 2026

By Sean Ring