Posted June 02, 2021

By Sean Ring

Credit Ratings and Old Flames

Whats the number between 5 and 7?

Sex!

Back in 03, I was living in London and dating a Kiwi.

No, not the fruit. She, who will not be named, hailed from Dunedin, on the South Island of New Zealand. A statuesque 60 to my mere 510, she was a fitness freak and avid sportswoman, with curves in all the right places.

If you dont have any Kiwi friends, you wouldnt know they dont pronounce six properly. Or that eggs are iggs. Its a funny accent. Australians loathe Americans who mistake them for Kiwis.

She and I were like oil and water - I long preferred the pub to the gym. Despite this, it was a rip-roaring two-month whirlwind of an affair.

Crucially, I learned an important lesson from her: theyre all in bed together.

Credit Ratings Agencies and Banks

She worked for one of the largest credit ratings agencies as an Associate Director in Structured Finance. I was a mere futures broker for my favorite Swiss bank. I didnt pretend to understand what she really did at her day job. But curiosity got the better of me one night over dinner and I asked.

As nearly two decades have passed since that night, Ill paraphrase as best as I can. Please also keep in mind that this was long before the real estate market blew up in 2006.

Darling, what exactly do you do?

Well, big American investment bank called me today.

Wait, they just called you up?

Yeah. Pronounced yee in Kiwi.

And what did they say?

Well, they needed a tranche rated triple-A.

Pause: a tranche is a slice in French. Simply, banks would package up mortgages into Mortgage-Backed Securities (MBSs). Then they'd slice them into tranches to sell to various institutional buyers. They sliced up all sorts of stuff, and still do, ranging from credit cards to student loans to auto loans and beyond.

As an aside, youd be surprised how much the French mathematician/traders have to do with quantitative finance. Well, until you find out most of them went through the prpas, which is the most intensive post-secondary training in Europe. Plainly speaking, these frogs are math freaks.

Now back to our conversation.

Ok, so big American investment bank just calls you and asks for a AAA rating?

Yeah.

And you just give it to them?

No. I run it through my models first. And if my models pass it, then I stress test it. If the stress tests are ok, then I give them the AAA.

Thanks to the primitive nature of those models, far too many slipped past the credit ratings agencies into AAA status. Nassim Taleb wrote on this extensively at the time and thats why he was able to call the crisis so accurately.

I was utterly dumbfounded. It didnt make sense to me that a huge bank would call up a ratings agency and ask for a rating. Whats more, the bank would then pay the ratings agency for the rating.

Im not accusing her of any wrongdoing at all. To the envy of most businessmen, including Jeff Skilling, she was as pure as the driven snow. Except in bed, when I felt like I was wrestling a Navy SEAL.

Back then regulators encouraged ratings agencies to talk to banks to see what they needed. In England, thats called being commercial and its the kind of conduct that Credit Suisse recently demonstrated with Greensill and Archegos, much to the chagrin of their shareholders.

We all know what happened in 2006, largely thanks to the coziness of this relationship.

There Are No Circuit Breakers in This Market

If you havent watched the documentary Inside Job, Ill quickly summarize for you why the US real estate market became a worldwide problem.

Its easy to blame the big investment banks for packaging subprime mortgages and selling them to international investors. But lets take a step back and see the big picture.

Mortgage brokers were happy to lend to people who qualified only for NINJA mortgages. NINJA, of course, stood for No Income No Job no Assets. Those mortgages had teaser rates for the first 3 years, making it look like those poor borrowers were getting the best deal ever.

Even in a low rate era, these people had practically no chance to pay back the principal on their mortgages.

But mortgage brokers werent worried, because mortgage bankers would surely reject those cases. Except they didnt, because they knew large international banks would put a check on them.

Except the large international banks didnt put a check on them at all. Thats because large international banks knew they could package these mortgages - with the uncritical help of the credit ratings agencies - into MBSs and sell them to their international clientele.

The international clientele was left holding the bag once Helicopter Ben Bernanke, lately of the Federal Reserve, decided to raise interest rates.

The staircase on the above graph is when Helicopter Ben and his FOMC water-tortured rates up to 5.25%, sending those teaser rates well above the NINJA holders affordability.

To remind you, the FOMC is the Federal Open Market Committee, the band of merry men and women who attempt to control interest rates.

In effect, the Fed popped the bubble by taking away the punch bowl. Its an error (or was it) Jay Powell and his crew are keen to avoid.

Will Credit Ratings Agency Really Downgrade Banks on Weak Governance?

A friend of mine referred me to a Forbes article written last week titled, Financial Institutions Are On Notice That Weak Governance Can Lead To Ratings Downgrades And Significant Fines.

Despite Credit Suisse getting a downgrade for a very public display of sheer stupidity, Goldman Sachs escaped a downgrade for the multibillion dollar scandal with 1MDB. It was deemed that the Goldman case wasnt a systemic breakdown of corporate governance or the firms risk management infrastructure.

Id allege its because most Americans couldnt find Malaysia on a map nor care to do so.

I dont doubt the authors sincerity. But Im reminded of Charlie Mungers famous quote, Show me the incentive, Ill show you the outcome.

The fact remains that banks pay credit ratings agencies for their ratings. So, the ratings agencies are incentivized to keep their banking clients happy.

I think that means downgrades will come much slower than they otherwise would have, had the fee structure been fixed after the 2008 crisis. It never was.

In fact, not much has changed since 2008. And thats the issue. Not only did we not learn from that crisis, we actively ignored the lessons it taught us.

Well, not all the lessons, I suppose. These days, I remember them over a nice glass of Cloudy Bay.

Until next time!

All the best,

Sean

The Magnet That Breaks China’s Grip

Posted August 07, 2026

By Matt Badiali

The Situational Awareness Paradox

Posted August 06, 2026

By Sean Ring

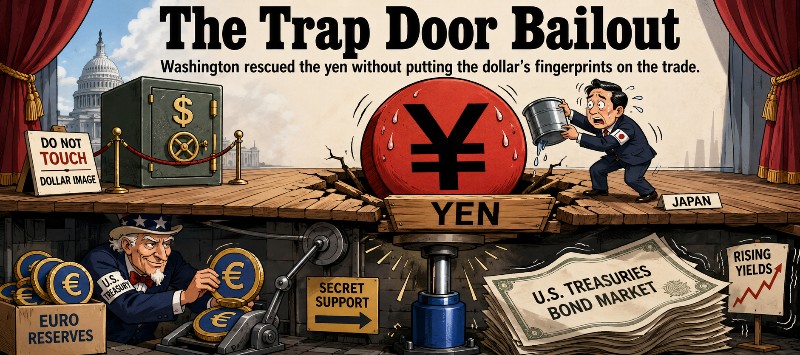

The Trap Door Bailout

Posted August 05, 2026

By Sean Ring

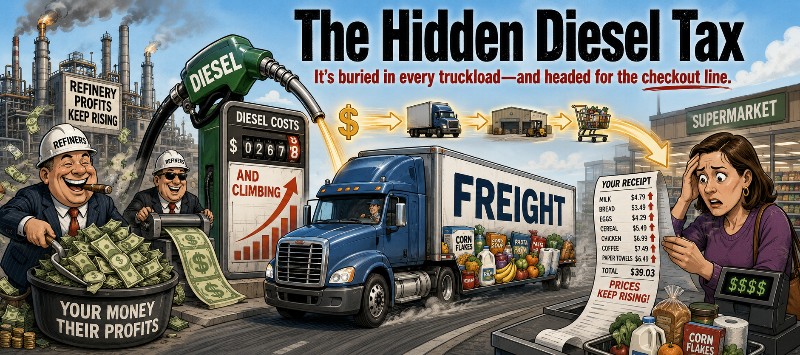

The Hidden Diesel Tax

Posted August 04, 2026

By Sean Ring

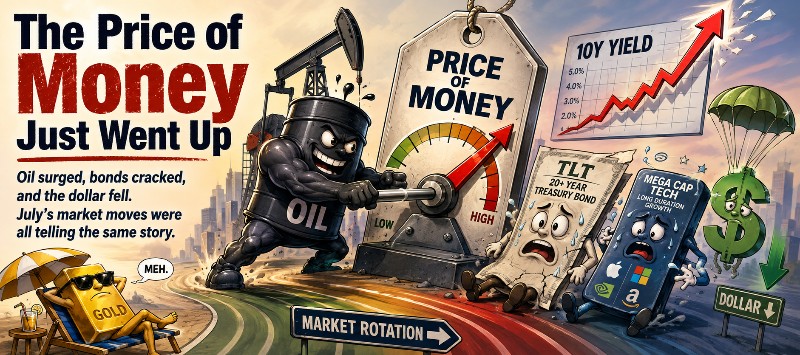

The Price of Money Just Went Up

Posted August 03, 2026

By Sean Ring