Posted April 20, 2026

By Sean Ring

Bull Trap Snaps Shut?

Here's the contradiction of the moment.

Bank of America's April fund manager survey just came out. It shows the most bearish mood since June 2025. Allegedly, the big money is terrified.

And yet those same fund managers just dumped $172.2 billion of cash into the market. That's the biggest April cash outflow from money market funds on record.

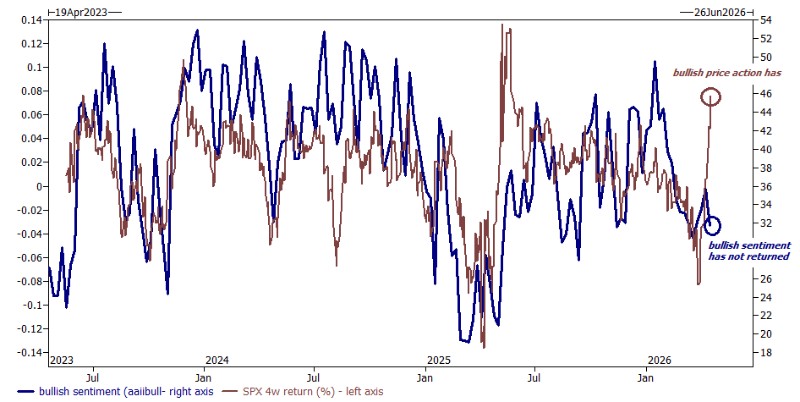

Watch the hips, not the lips. Fund manager sentiment doesn’t reflect the price action. Credit: Zero Hedge

Watch the hips, not the lips. Fund manager sentiment doesn’t reflect the price action. Credit: Zero Hedge

For some perspective, the average April outflow over the last four years was $41 billion. Last year it was $103 billion. This year? $172 billion, though some of it was for tax purposes.

They say they're scared. They lie… because their allocations tell us otherwise.

This is what a bull trap looks like from the inside.

Before we move forward, let’s define a bull trap. It’s a false trading signal in which a declining stock or market index briefly rallies, breaking above a key resistance level (in this case, an all-time high), only to reverse abruptly and resume its downward trend.

The Rally That Smells Wrong

The Nasdaq just logged 13 straight up days. That's the longest winning streak since July 2009.

The S&P 500 went from oversold to overbought in just 11 trading days. According to BofA's Michael Hartnett, that's the second-fastest shift of its kind since 1982.

It’s a short squeeze in a party hat.

Short sellers got blown out. The trend-following funds (CTAs, in the jargon) flipped from short to long. And now that all the forced buyers are done buying, here's the question:

Who's left?

Follow the Money… Out the Door

Look at where the cash actually went.

Of that $172 billion, $11.3 billion went into stocks. Of that, $17.4 billion went into US stocks. (Yes, more into US stocks than into stocks overall, because investors pulled capital out of everywhere else.)

Another $7.9 billion went into bonds. Gold and crypto each got $1.2 billion. Junk bonds got $3.1 billion, their biggest haul since May 2025.

Treasuries had outflows for the first time in eleven weeks, and who can blame the sellers? With The Donald wanting Fed cuts and a weaker dollar, I’m not a fan.

Now look at what got sold:

- Emerging markets: down $10.5 billion

- Europe: down $4.7 billion

- Japan: down $4.4 billion

- China: down $10.8 billion

- Korea: down $2.5 billion (a record)

- US Tech stocks: down $3.8 billion

This is less a risk-on rally than a stampede into US stocks from everywhere else on Earth. And how do stampedes usually end?

The Hormuz Head-Fake

By the way, welcome to Week 8 of “2 weeks to flatten the Iranians.”

Friday showed you how fragile this all is.

Iran's Foreign Minister had reportedly said the Strait of Hormuz was "open." The S&P sprinted to a fresh high above 7,100. Oil crashed 12% to $83. Buy everything!

Then the weekend happened.

Like most weekends before it, we’ve seen some selling after a great Friday gift to the markets, usually in the form of The Donald declaring “Mission Accomplished!” for the umpteenth time.

That's the texture of a bull trap. Violent headline moves that can't stand on their own legs. The market wanted to believe. It found a reason. Unfortunately, the reason wasn't real.

Leverage: Loaded and Pointed Nowhere

Goldman Sachs' John Flood, who runs US trading, wrote over the weekend that the market feels "stretched" and is "fully prepared for a pullback."

Here's why.

Across Goldman's prime brokerage, gross leverage sits at 310%. That's the 98th percentile over five years. Put simply, for 98% of the last five years, hedge funds were less levered than they are right now.

But net leverage is only 75%. That's the 21st percentile.

What does that mean? The big funds have piled on huge long and short bets simultaneously. They're crowded. They're coiled.

When a market is wound this tight, it usually snaps rather than sells off calmly.

Goldman's Brian Garrett put it this way: the short-covering and trend-follower buying is over. Earnings season will be the real test.

That means the bots are done buying. Now companies have to deliver.

What Hartnett Is Watching

Here's Hartnett's roadmap for what comes next:

- CPI and earnings estimates peak in Q2

- The 2-year Treasury yield fails to break above 4%

- The yield curve keeps steepening

- The dollar index (DXY) makes a new low below 96

- China's Shanghai Composite heads to 4,500

His favorite trades? Commodities (they hedge risk, inflation, and a weak dollar at once). And Chinese stocks — especially the ChiNext index, which he sees breaking out.

The ChiNext Index covers 100 of the largest and most liquid A-shares on the ChiNext board, weighted by free-float market cap. It’s the Shenzhen Stock Exchange’s NASDAQ-like market for high-growth tech companies.

Goldman likes tail-risk hedges right now. Three-month puts on the S&P are cheaper than they were before the Iran conflict. That's an odd anomaly given where we are in the cycle.

And for the bulls? Upside volatility is cheap enough that a 2–3% further rally could trigger a "gamma squeeze" where market makers are forced to buy more as prices rise. That would cascade into a final blow-off top. No doubt our options guru Nick Riso will be watching.

There's also a fertilizer trade brewing. Goldman sees Middle East supply problems spilling into grain markets for another six months. That means fertilizer prices stay bid.

Wrap Up

The bears' real worry isn't complicated. It's that inflation hasn't peaked.

If oil bounces back in Q2, CPI ticks higher, and the bond market reprices, we may get a rerun of the 2022–2023 horror show. Stock multiples compress. Credit spreads widen. The trade everyone crowded into becomes the trap no one saw coming.

Let's tally the scoreboard:

Annual global equity inflows for 2026 are on pace to top $1 trillion. The most bearish fund manager survey in almost a year. A 13-day Nasdaq streak. Leverage at 98th-percentile extremes. And a rally triggered by a headline that turned out to be fake.

The trap is set.

History’s Greatest Bar Bill

Posted July 31, 2026

By Sean Ring

The Bond Market’s Fed

Posted July 30, 2026

By Sean Ring

Sacrifice Arbitrage

Posted July 29, 2026

By Sean Ring

The Last Great Crack

Posted July 28, 2026

By Matt Badiali

The Consent Nobody Gave

Posted July 27, 2026

By Sean Ring