Posted October 29, 2024

By Sean Ring

2 Worrying Signs No Matter Who Wins

In between the Democrats calling Trump “Hitler” and the Republicans calling Harris “low IQ,” there are some worrying signs for the economy that whoever wins will have to deal with.

The big issue with these problems is they aren’t easily solvable. Markets are global nowadays, so a swift stroke of a politician’s pen does nothing.

These aren’t just domestic issues, either. Politicians should consider these “events” and treat them as such. Sure, policy has caused these events, but the toothpaste is out of the tube. Now, every move they make may exacerbate the problem.

Let’s walk through what I think are the two most pressing economic conundrums:

The Price of Oil

You may be thinking, “Hey, cheap oil is good!” I’d normally agree with you.

But let’s conduct a thought experiment.

Let’s go back a mere fifteen years ago. I tell you the following:

There is a war raging on the Russia/Ukraine border. NATO is supplying the Ukrainians, while Russia is pretending it’s not so it doesn’t escalate the situation. Hamas invaded Israel a year ago when Bibi left the southern border unguarded, but the problem has spun entirely out of control. Iran is now actively involved, and Israel and Iran have traded blows directly. Houthi rebels have shut down the Suez Canal. Now, shipping traffic is traveling the same route Vasco da Gama did. America is worried China will invade Taiwan, so it’s building TSMC foundries in the US. Due to a pandemic blown entirely out of proportion, supply chains still haven’t recovered from a worldwide government-mandated private-sector shutdown. Inflation in the United States reached 9.2% year-on-year in 2023 but has settled down around 3%.

What do you think oil trades at?

My guess is that you’d say something like $150 to $200 per barrel. That’s what I think it “should” be trading at.

This morning, we’re at $68.30, less than half my low-end guess.

There are two ways to think about this: supply and demand.

Some of my colleagues argue that the US has become such a colossal oil supplier that it’s tamping down prices. I’m sure there’s merit in that argument.

But the balance of probabilities now resides with the demand side.

The Kobeissi Letter recently posted this on X:

2 weeks ago, the IEA cut their 2024 demand growth forecast yet again.

The IEA said world oil demand would rise by 40,000 less barrels per day than expected in 2024.

Consumption dropped by 500,000 bpd year-over-year in August, a 4th consecutive month of declines.

Most recently, OPEC cut its demand forecasts for oil demand growth in 2024.

OPEC said world oil demand will rise by 1.93 million bpd in 2024, down from growth of 2.03 million bpd it expected last month.

Chinese demand was a major driver.

But what about the stimulus in China?

China's stimulus has had a muted reaction thus far.

In Q3 2024, China saw their 6th consecutive quarterly decline in consumer prices, the longest streak since 1999.

The reality is that China is likely already in a recession and it's going to be a long road out.

We’re probably already in a worldwide recession. The stock market just hasn’t followed it yet.

In short, cheap oil isn’t the problem in and of itself. It’s what cheap oil is signaling that’s not great.

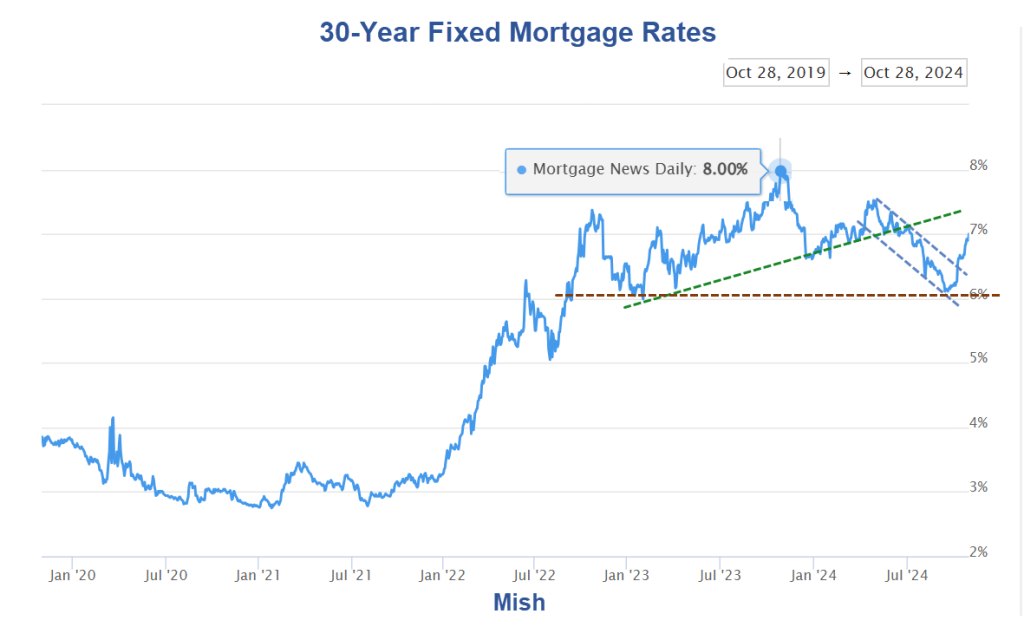

30-Year Fixed Mortgage Rate

Mish Shedlock posted an equally scary piece on mortgage rates:

Credit: Mish Shedlock

The Fed just cut rates by 50 bps, but mortgage rates are rising? Not good. Why is that?

When mortgage rates rise, the effects cascade throughout the economy.

Higher mortgage rates make homeownership prohibitively expensive for regular folk. Higher interest rates mean steeper monthly payments. With a larger share of income funneled into mortgage bills, prospective homeowners are priced out of the market. That same squeeze lowers buying power across the board, particularly affecting first-time buyers and those with lower incomes. This strain feeds into a cooling housing market as fewer people enter homeownership.

A subdued housing market also means stagnating or falling home prices. With demand suppressed by higher financing costs, the flow of transactions slows down, and as a result, house prices take a hit. While this might sound like good news for bargain-hunters, it’s brutal for recent buyers who suddenly find themselves owing more on their mortgage than their home is now worth. This is “negative equity,” a condition that restricts homeowners from moving or refinancing and is especially harsh for anyone who purchased at peak prices.

As fewer people buy, we see knock-on effects that extend far beyond property values. For one, decreasing housing demand causes a drop in new construction projects. Builders are reluctant to launch new projects in an economic environment with few buyers, limiting the housing stock and curbing development in growth-focused regions. Compounding the issue, fewer homes on the market increase rent as more people opt to lease instead of buy.

This belt-tightening bleeds into the broader economy. With a larger slice of household budgets going to housing, there’s less cash left over for discretionary spending. Local businesses feel the impact as families cut back on dining, entertainment, and retail.

Families with adjustable-rate mortgages (ARMs) feel the pinch acutely. Rate hikes that drive monthly payments higher strain household budgets, putting many at risk of missing payments or even facing foreclosure if rates spike dramatically.

This instability seeps into financial markets, affecting real estate and mortgage-backed securities portfolios. Banks with high exposure to real estate loans would tighten lending, wary of defaults. Those tightening credit conditions can reduce access to financing across sectors, creating further headwinds for small businesses and investors who rely on loans to sustain and grow their ventures.

Home equity has long been a reliable path to financial security, but as entry barriers rise, fewer people benefit from this vehicle.

High mortgage rates are a fundamental barrier to growth and wealth for most people. They drive a wedge into real estate, whether it’s the neighborhood, your investment portfolio, or the broader economy.

Wrap Up

The good news is that oil is cheap. The bad news is that this means a recession is either here or inevitable.

With the Fed cutting rates but mortgage rates still rising, the economy is on edge.

Whether it’s The Donald or Kamala, the next president has their hands full.